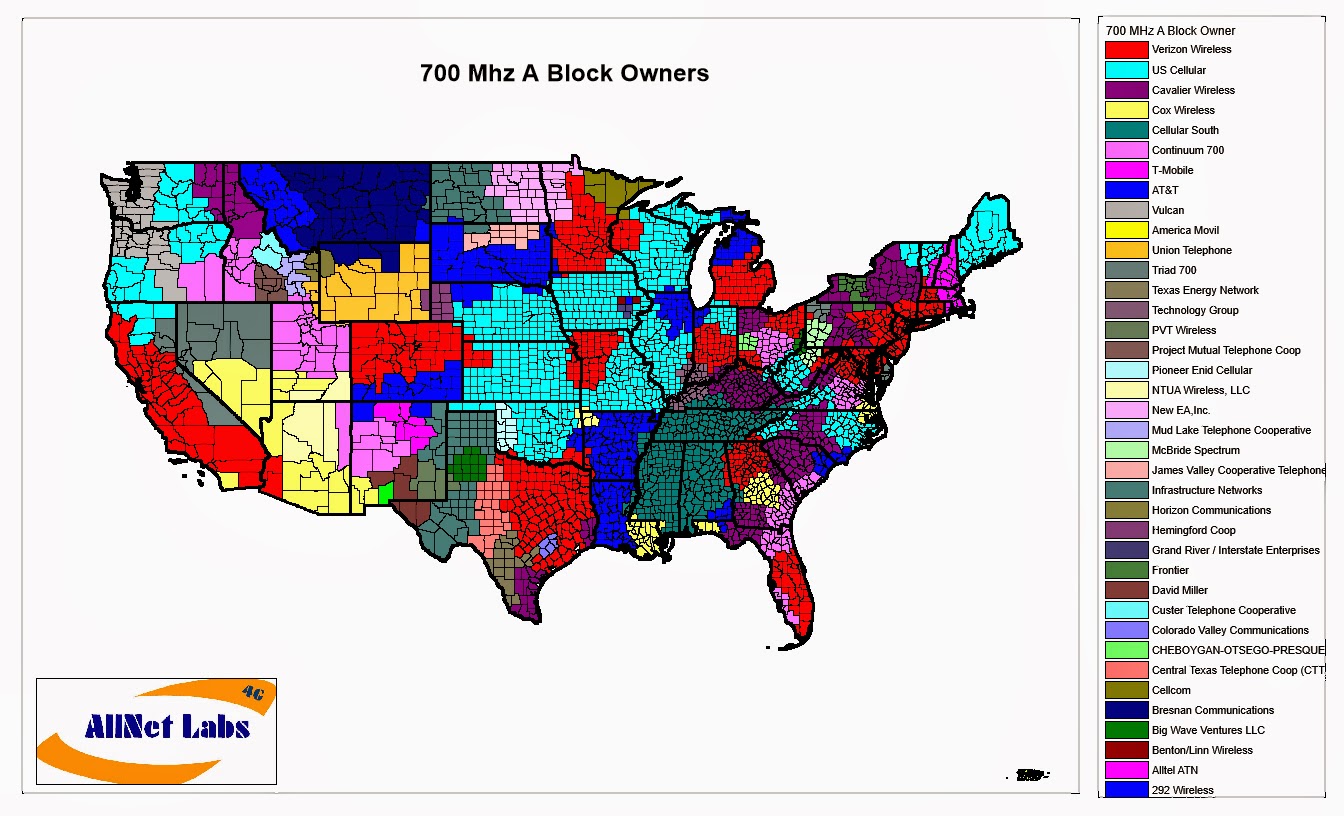

With the recent industry press indicating that T-Mobile was positioning its self to purchase Verizon's 700 MHz A Block, I decided to dive into the Spectrum Analysis Tool to see what kind of geographic area Verizon's licenses would provide T-Mobile with low band spectrum.

Clearly it would not be a spectrum purchase to provide coverage in rural areas since it doesn't address the rural areas in the western United States with the exception of western Colorado. Looking at it on a Cellular Market (CMA) basis, this spectrum would provide T-Mobile with low band spectrum in all 15 of the Top 20 markets but only 25 of the Top 50 markets. This includes both the Verizon spectrum and T-Mobile's 700MHz spectrum acquired from MetroPCS.

To acquire the remaining 700 MHz A block spectrum in the Top 20 markets, T-Mobile will need to be talking to:

Leap - Chicago

US Cellular - St. Louis

McBride Spectrum - Pittsburg

Cox - San Diego

Vulcan - Seattle

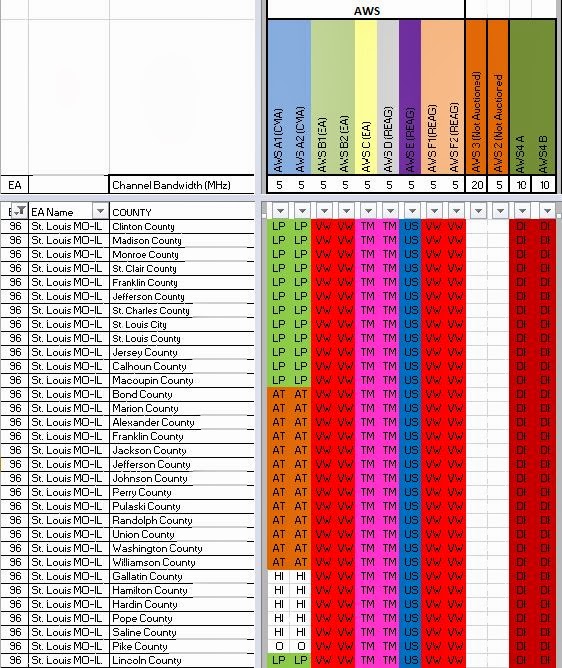

It is interesting to look at the details of Verizon's spectrum purchase from US Cellular in the St Louis market area (EA-96). Many industry sources talk about how purchase will provide 20MHz for Verizon's LTE. While this is true, it should not be confused with Verizon deploying a 20 x 20 channel. As can be seen from the Spectrum Grid view of AllNet Labs' Spectrum Ownership Analysis Tool, Verizon is purchasing the AWS B channel and previously owned the F channel. Although Verizon will own 20 MHz of spectrum, it is not contiguous and until they can deploy Release 12 software code into their network, they will have to operate this spectrum as two separate 10 MHz channels. Release 12 is likely a 2015 or maybe 2016 release since operators are either planning or deploying Release 10 currently.

The industry talks alot about Carrier Aggregation (CA) but there are several facts that are not well understood. First, Release 10 includes the functionality for carrier aggregation but the frequency band definitions for the US are not included until Release 11. Another point that needs to be understood is that the initial definitions require that aggregated carriers be in contiguous blocks in different spectrum bands (inter-band) or in separate blocks but in the same band (intra-band). For Release 11, only 2 carriers can be aggregated together. For Release 12, Verizon has sponsored a work group that will allow 3 carriers to be aggregated, 1 from the 700MHz band and 2 different carriers from the AWS band. Thus, Release 12 will be necessary for Verizon to aggregate their two AWS blocks of spectrum with their 700 MHz LTE.

The Spectrum Grid view is sorted by the EA geographical area which show that the AWS B and C licenses have not be dis-aggregated. The A channel licenses do show discontinuity since they were originally auctioned as CMA licenses. AT&T through their Leap purchase will strengthen their AWS ownership in this market.

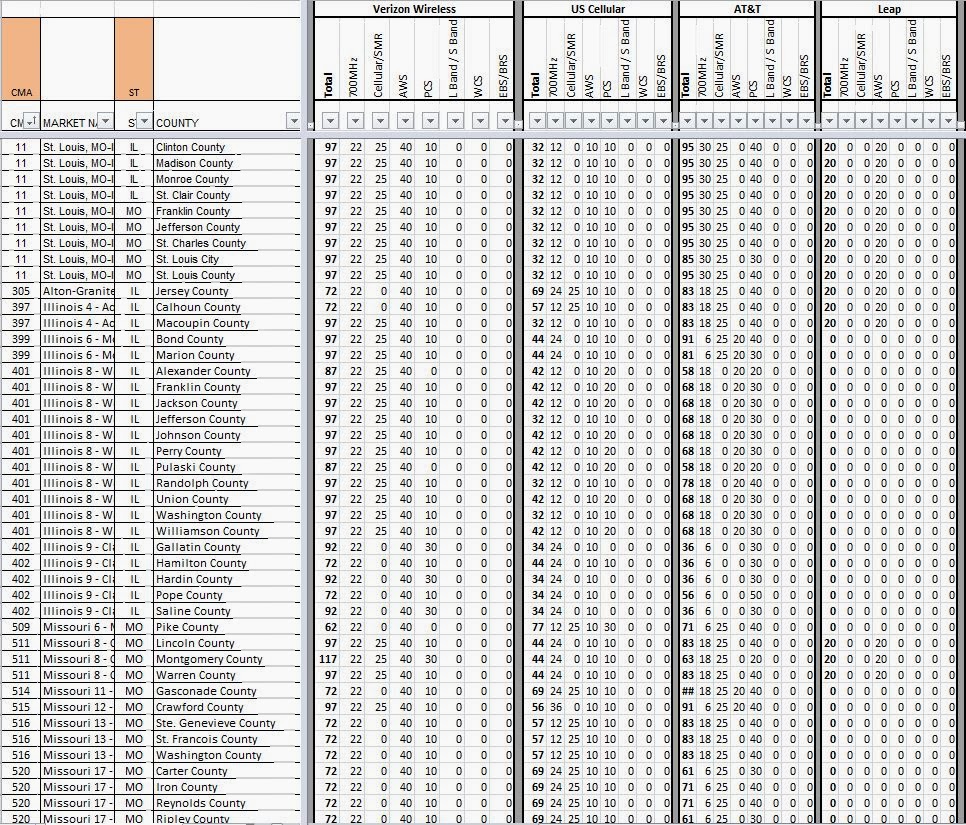

To look at the competitive picture for spectrum in the St Louis market (EA-96) we can look at the

Company By Band worksheet from the AllNet Labs' Spectrum Ownership Analysis Tool. Looking first at Verizon, we can see the variety of spectrum depths across the EA that Verizon indicated in their FCC filing. Verizon will range from 62 MHz to 117 MHz depending on the county. The only county that Verizon controls 117 MHz is Montgomery County, MO which is 40 miles west of St. Louis.

Looking at the other carriers in this market we see that US Cellular will still control between 32 MHz and 69 MHz, while AT&T with their Leap purchase will control between 61 MHz and 105 MHz.

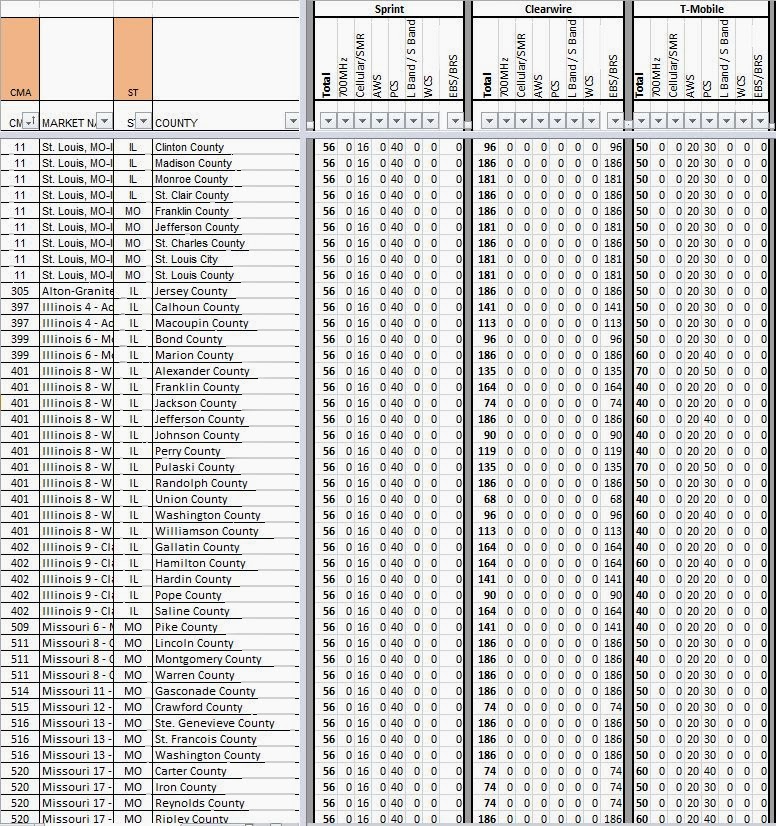

T-Mobile controls between 40 MHz and 60 MHz with two counties at 70 MHz and Sprint with their Clearwire purchase controls between 130 MHz and 242 MHz.

T-Mobile announced an acquisition this morning of USCellular's AWS spectrum in several markets. This was clearly foreshadowed when I analyzed the Sprint - USCellular PCS spectrum deal earlier this year.

On this chart from the Spectrum Ownership Analysis Tool, you can see the PCS spectrum in Chicago and St. Louis that Sprint acquired along with the subscribers and network. Thus it was clear to see that USCellular's AWS(B) and AWS(E) spectrum was no longer needed.

It clearly makes sense for T-Mobile to acquire this spectrum as indicated in the chart below. In St Louis, T-Mobile will increase their LTE Channel size from 10MHz to 25MHz and in Kansas City, T-Mobile will increase from 10MHz to 15MHz. The chart also highlights the important spectrum position that Leap hold in the AWS band which both T-Mobile and Verizon would desire to add to their portfolio.

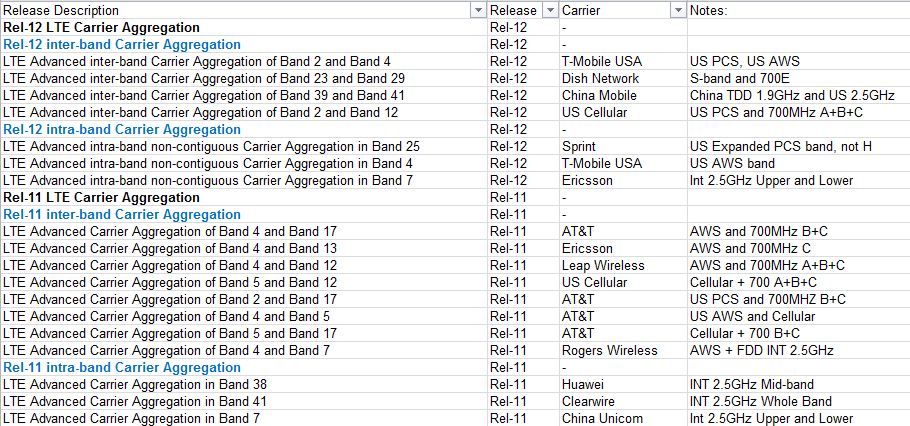

Recently I reviewed the 3GPP Standards site to check in on the status of LTE Carrier Aggregation. I found a gold mine of information.

First a few definitions: Carrier Aggregation allows a wireless carrier to band together different blocks of their spectrum to form a larger pipe for LTE. This can be accomplished in two ways: Inter-band and Intra-band.

Inter-band combines spectrum from two different bands. The spectrum in each band to be combined must be contiguous within that band. Intra-band combines spectrum from two non-contiguous areas of the same band.

Here is a link to an article from 3GPP that explains Carrier Aggregation.Below is a table summarizing the relevant 3GPP working group descriptions for Carrier Aggregation.

First of all, the current network release for all carriers is Release 9. T-Mobile, Sprint, and Clearwire have announced that they are deploying Release 9 equipment that is software up-gradable to Release 10 (LTE Advance). From the chart, it does not appear that there are any carrier configurations planned until Release 11. Release 10 appears to be a late 2013 commercial appearance and Release 11 will likely be very late 2014 or mid-2015. For Carrier Aggregation to work it must be enabled and configured at the cell site base station and a compatible handset must be available. The handsets will transmit and receive their LTE data on two different spectrum bands for the Inter-band solution. All handsets currently only operate in one mode, 700MHz, Cellular, PCS, AWS, or 2.5GHz.

Highlights by Carrier:

Canada: Rogers Wireless will have support for inter-band aggregation between their AWS spectrum and the paired blocks of 2.5GHz spectrum.

AT&T: Inter-band support in Release 11 for their Cellular and 700MHz spectrum, inter-band support to combine their AWS and Cellular spectrum, as well as configuration to support combining their PCS and 700MHz spectrum. All of the 700MHz band plans only include their 700B/C holdings. No 700MHz inter-operability.

USCellular: Inter-band support in Release 11 for Cellular and 700MHz (A/B/C). No support for PCS or AWS spectrum combinations

Clearwire: Intra-band support for the entire 2.5GHz band. China Mobile is also supporting this with an inter-band aggregation between 2.5GHz and their TDD 1.9GHz spectrum.

Sprint: Support in Release 12 for combining (intra-band)their holding across the PCS spectrum, including their G spectrum but not the un-auctioned H spectrum. No band support for their iDEN band or the 2.5GHz band.

T-Mobile: Support in Release 12 for intra-band in the AWS band and inter-band between AWS and PCS.

Verizon: Ericsson appears to be supporting Verizon's need to combine (inter-band) between AWS and 700MHz C. Not support for Verizon's Cellular or PCS holdings.

Dish: Release 12 support to combine their S band (AWS4) spectrum (inter-band) with the 700 MHz E holdings. This is the only aggregation scenerio for the US that combines FDD operation (AWS4) with TDD operation (700MHz E).