Free Shipping On world wide

- HOME

- PRODUCTS

- IN THE NEWS

- SPECTRUM BLOG

- WEB SPECTRUM VIEWER

-

English

-

USD

Free Shipping On world wide

Last week, Verizon filed applications to acquire the 28GHz (LMDS) spectrum held by two additional companies; Sunshine LMDS and Virginia Tech Foundation. We are using our recently released, Web Spectrum Viewer - Mapping Module to illustrate the spectrum owned by each of these companies. As with Verizon's other recent 28GHz acquisitions these transactions involve the Local Multipoint Distribution Service (LMDS) spectrum that was owned prior to Auction 101. The first map below illustrates the license area for Sunshine LMDS. Verizon is only acquiring the L1 and L2 channel spectrum from Sunshine LMDS. The spectrum depths on the map indicate that Sunshine controls the L1/L2 channels (850MHz) and the remaining A block LMDS channels (300MHz). The county detail for Sunshine's spectrum is indicated in the second map.

Sunshine LMDS:

Sunshine LMDS - County Detail:

The second transaction involves Virginia Tech Foundation. In this transaction, Verizon is acquiring rights to both the L1/L2 channels as well as the remaining A block LMDS spectrum. In the county detail map, the counties where Virginia Tech only controls the L1/L2 channels are visible in light tan color, while the markets where they also control the remaining A block LMDS channels are in a dark tan. The FCC controls the remaining A block LMDS channels in the counties where Virginia Tech Foundation only controls the L1/L2 channels.

Virginia Tech Foundation:

Virginia Tech Foundation - County Detail:

In July, the FCC released their report and order for their plans to auction the white space 2.5 GHz spectrum. Using our Mobile Carrier - Spectrum Ownership Analysis Tool we have created a couple of images to illustrated the auction of the spectrum in a rural county and the auction of spectrum in a urban county.

Our rural example focuses on Wayne County, Iowa. Wayne County has a population of nearly 6,500.

In the image above, we indicate the primary spectrum ownership for each channel in Wayne, IA. Sprint is the spectrum owner for all of the BRS (Broadband Radio Service) channels and the FCC is the spectrum owner for all of the EBS (Educational Broadcast Service) channels. We have highlighted in the Bandwidth row, the different channels the FCC has defined for auction. The red highlights are for the 49.5MHz channel, the green highlights indicate the channels included in the 50.5MHz channel and the blue highlights indicate the channels included in 17.5MHz channel. The 17.5MHz channel consists of 3 x 5.5MHz contiguous channels and 3 x 0.33MHz guard band channels.

In the area below each channel we indicate in green, the available population that can be licensed for each channel as a percentage. Clearly, purchasing any of the 3 channels (49.5, 50.5, 17.5) at auction would provide a carrier with the ability to service 100% of the population with each of the component 2.5GHz channels.

Our urban example focuses on McHenry County, IL. McHenry County has a population of nearly 310,000. McHenry County is one of the 6 counties that constitute the Chicago CMA Market.

In the urban example, the carrier that purchases the red (49.5MHz) channel would be able build a network reaching 20% of the population with the A1, A2, and A3 channels (16.5MHz), they would be able to reach 80% of the population with the B1, B2, B3, and C3 channels, and they can reach the entire population with the C1 and C2 channels. The auction winning carrier will have to coordinate their operations for all but the C1 and C2 channels around the geographic license areas that Sprint already controls.

Today, the FCC released results for Auction 101 (28 GHz) and Auction 102 (24 GHz). These results are now posted in our Millimeter Wave - Spectrum Ownership Analysis Tool. The Spectrum Ownership Analysis Tool provides 19 analysis modules to analyze each carrier's ownership in each of the millimeter wave bands. These modules include a spectrum ownership grid (below), seven different spectrum depth analysis modules, a MHz-POPs analysis module, and 3 licensed POPs analysis modules.

To summarize some of the auction results, we updated pie charts that were originally published in partnership with Fierce Wireless. These charts represent each carrier's MHz-POPs in terms of the country total.

24GHz:

28GHz;

39GHz:

As Auction 102 completes its 64th round today, I thought it would be a good time to share a map indicating the markets (PEA) where existing licensees already control spectrum prior to the start of the Auction 102. As you can see below, the FCC doesn't control 100MHz of the 24GHz spectrum in Reno (PEA076), Las Vegas (PEA026), and Phoenix (PEA015). The FCC also doesn't control 25MHz of spectrum in Albuquerque (PEA075). All of these licenses originally were controlled by M&M Brothers LLC and they track back to the original 40x40MHz channelization of the 24GHz band. M&M Brothers agreed to trade in their Casa Grande (PEA126), Saint George (PEA229), Gallup (PEA285), Socorro (PEA323), and Deming (PEA375) licenses for 100MHz licenses in the 3 yellow PEAs and a 25MHz license in the blue. Skyriver Spectrum & Technology now controls M&M Brothers licenses.

While the national map indicates the available spectrum depth on a PEA basis, our Spectrum Grid Analysis Module details the specific channels and counties that make up each of the PEA license assignments. In the Spectrum Grid, you can see complete ownership of channel 7 for all of the counties in PEA 15, 26, and 76; with on 25MHz in the two New Mexico counties.

On March 21st, the FCC released a Notice of Procedures describing how existing 39GHz spectrum ownership below will be remapped to the new 39GHz configuration. We thought it would be beneficial to see how the FCC arrived at their results.

Current Configuration:

Future Configuration:

The procedures the FCC announced will provide a route for the existing 39GHz owners to essentially trade-in their spectrum for vouchers that can be used in Auction 103. The FCC published a summary of the aggregated holdings data for each of the 39GHz licensees so we decided to use the data from our Millimeter Wave - Spectrum Ownership Analysis Tool to show the underlying calculations.

We are able to use the data from our Millimeter Wave - Spectrum Ownership Analysis Tool to determine the aggregate MHz-POPs value for PEA003 (Chicago). To find the aggregate MHz-POPs we must first find the MHz-POPs contribution for each of AT&T's licenses (call signs) in the Chicago market. Below are each of the county MHz-POPs components for each call sign. We have indicated whether the license covers the entire county or whether it is a partial license in the Full/Partial County column. The county MHz-POPs component is found by multiplying the bandwidth for each call sign by the county population. The total aggregate MHz-POPs is the sum of the county MHz-POPs for all of AT&T's licenses. Using this process, we have found AT&T's aggregate MHz-POPs to by 2,817,188,800 compared to the FCC's results of 2,815,434,000.

| Market | CallSign | Channel Block | Full/Partial County | State | County | Bandwidth | County Population | MHz-POPs |

| PEA003 | WRBI252 | 1A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 |

| Chicago | DuPage County | 50 | 916,924 | 45,846,200 | ||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI253 | 1B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI590 | 4A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI591 | 4B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBJ298 | 8A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBJ299 | 8B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBK275 | 13A | Partial | IL | Kane County | 50 | 21,235 | 1,061,750 | |

| Kendall County | 50 | 13,076 | 653,800 | |||||

| McHenry County | 50 | 37,438 | 1,871,900 | |||||

| 13B | Partial | IL | Kane County | 50 | 21,235 | 1,061,750 | ||

| Kendall County | 50 | 13,076 | 653,800 | |||||

| McHenry County | 50 | 37,438 | 1,871,900 | |||||

| 2,817,188,800 |

The Market MHz-POPs value is found by multiplying the new 39GHz channel size (100MHz) by the total population of the Chicago PEA.

| Market | Bandwidth | PEA Population | Market MHz-POPs |

| PEA003 (Chicago) | 100 | 9,366,713 | 936,671,300 |

The next calculation provides the number of blocks that AT&T is authorized to receive in the 39GHz auction by relinquishing their current licenses. Our analysis indicates that AT&T will start with slightly more than 3 - 100MHz channel blocks in Chicago before the auction starts.

| Market | Aggregate MHz-POPs | Market MHz-POPs | Channel Blocks |

| PEA003 (Chicago) | 2,817,188,800 | 936,671,300 | 3.00766 |

To determine how much Millimeter Wave spectrum is controlled by the FCC, we utilize the National & State Market Analysis module from our Millimeter Wave - Spectrum Ownership Analysis Tool. The values below are calculated as population weighted averages of the FCC's controlled spectrum at the county-level. On average, the FCC has nearly 3500 MHz of spectrum available. Most of that spectrum (2700 MHz) is coming from the newly identified spectrum bands (37GHz and 47GHz) along with the reconfigured and expanded 24GHz.

On April 19th, the FCC opened a docket to collect comments related to "Transforming the 2.5 GHz Band". As background, the US 2.5GHz spectrum band encompasses 33 channels. 20 channels (A, B, C, D, and G groups) are designated for Educational Broadcast Service (EBS) and 13 (BRS1/2, E, F, and H) are designated for Broadband Radio Service (BRS).

License Area:

Sprint owns a vast majority of the BRS licenses and leases a vast majority of the EBS licenses. The licensing limitations for this spectrum are drawn from its origins providing broadcast video services. The original licenses were formed as 35 mile radius circles centered on the video transmitting site. When two licenses overlapped, a football shaped area would be formed. A line would be drawn through the end points of the "football" splitting the overlapping license area between the two licensees. BRS licenses include both 35 mile radius licenses, geographic area licenses (entire BTA) and Entire BTA license with cutouts for existing 35 mile radius licenses.

In 2009, a Broadband Radio Service auction (Auction 86) included the remaining unlicensed areas within each BTA for the BRS channels, but the unlicensed area in each BTA for the EBS channels was not auctioned.

Channel Plan Transition:

Prior to this point, Clearwire was launching pre-WiMax networks on the EBS/BRS pre-transition band plan which was designed around video operation. As you can see in the Pre-Transition chart below, the A channels (A1, A2, A3, and A4) are separated by the B channels (B1, B2, B3, and B4). This allowed all of the A channels to be broadcast at a video site without interference. Clearwire would need to control both sets of the "interleaved" channels to have enough contiguous spectrum to launch their RAN network in a market.

To facilitate data network deployments and to protect the remaining video operations the FCC provided a way to transistion licenses to the Post-Transition band plan on a BTA market basis. If there was a significant commercial video operation in a market, that BTA market was able waived from transition and it stayed with the Pre-Transition band plan. The Post-Transition band plan put the remaining video operators into the mid-band segment (A4, B4, C4, D4, G4, F4, and E4) and provides contiguous spectrum (16.5MHz) for the rest of the channel group (e.g. A1, A2, and A3)

FCC Request for Comments:

License Area:

The FCC has expressed a desire to make the EBS unlicensed area available for use. The FCC has asked whether the expansion of the licenses should include the entirety of the census tracks that license (35 mile) intersects or the entire county that the license intersects. The map below from the National EBS Association (NEBSA) illustrates the counties that would be added to each intersecting EBS license for the A1 channel. For the carriers that already lease these licenses, they would have the opportunity to deploy sites on the larger license area and would likely also pay the licensee a higher monthly payment due to the increase in licensed population. As you can also note below, this approach still leaves all of the white counties unlicensed.

The FCC would like to license the white counties in a 4 step manner:

Service Rules:

The FCC is also proposing to change the service rules for the EBS spectrum to allow the spectrum to be sold to commercial operators rather than requiring leases.

Remaining Pre-transition Markets:

The FCC is also proposing to complete transitioning the remaining pre-transition markets so a consistent band plan would be in use nationwide. A few wireless cable operators had received waivers but most of those operators have ceased operations. This will clear interference issues between markets and facilitate the deployment of data in the Lower Band Segment (A,B,C, and D groups) and the Upper Band Segment (E,F,G, and H groups). Video operations will continue in the Mid Band Segment (A4, B4, C4, D4,G4,F4, and E4) in the markets where they operate today.

In our last post we were discussing the next steps for the US millimeter wave spectrum after FiberTower and the FCC settled FiberTower's licensing issues. As we prepare for a 28GHz auction in November, and a 24GHz auction early next year, let's take a look at how each of the new millimeter wave frequency bands are configured. Each of these images is taken from our updated Millimeter Wave - Spectrum Ownership Analysis Tool which is now reflecting the new channel band plans for 24GHz, 37GHz, and 47GHz.

24 GHz Spectrum:

In this view we show both the expanded 24GHz band configuration and the old 24GHz configuration. All of the spectrum depth values are calculated from the New 24GHz data. We have left the old 24GHz configuration, so you can continue to see the remaining 24GHz spectrum licenses which will need to be moved over to the New 24GHz by the FCC. The current licenses are licensed for a 40MHz uplink and 40MHz downlink which won't map properly to the new band plan.

37GHz Spectrum:

For the 37/39GHz bands we show the new 37GHz band alongside the reconfigured 39GHz band. The new 39GHz columns are not populated because the existing spectrum holders will need to be transitioned to the larger/unpaired channels in the new 39GHz plan. We are providing spectrum depth values for the new 37GHz spectrum and the old 39GHz spectrum.

47GHz Spectrum:

We have added the new 47GHz band configurations to the Spectrum Grid and each of the spectrum depth modules.

PEA Market Analysis:

Our last addition, is a PEA Market Analysis module. This module displays spectrum depths for each selected carrier using the new FCC Auction market structure. For the 28GHz auction, you can see the amount of spectrum that will be available in each of the PEAs in the LMDS A (FCC) column on the far right of the chart.

In my most recent post on the filed FCC Transactions for February 2017 there were over 275 call signs that were assigned to new licensees and nearly 100 call signs that were leased. In an industry driven by spectrum, these changes affect the operations for every wireless carrier, they change site interference, and they affect the channels that are programmed into private repeaters and DAS systems.

So how can your company stay on top of the changes that may affect your markets. Allnet Insights' publishes a National Carrier Spectrum Depth Report which details the spectrum held by Verizon, AT&T, T-Mobile, Sprint, Dish, and USCellular in the Top 100 Cellular Market Areas (CMA). We report both the spectrum that each carrier currently holds (Current Holdings) and the spectrum they will hold in the future (Future Holdings) based on pending FCC transactions. Reporting on both current and future holdings enables Allnet Insights' to also report on the changes between current and future holdings which highlight the location and quantity of spectrum that is changing hands.

Below is a screenshot of the 11th through the 25th most populated CMA markets in our February 2017 report. This highlights the markets where the national carriers are either increasing or decreasing their spectrum holdings. In the Excel report you can reveal specific holdings by frequency bands that are changing but for this post, we will stay with the total spectrum view. From this view, you can see that in San Diego, T-Mobile is increasing their held spectrum by 5MHz while AT&T is decreasing their held spectrum by 5MHz. The reverse is happening in the Sacramento CMA.

We also highlight the spectrum that is changing hands in our Web Spectrum Viewer. In the Spectrum Grid menu, we lower case the 3 letter carrier code to indicate that the carrier ownership is changing from the current to the future. Looking at the same San Diego market (San Diego County) you can see (tmo) on the PCS B6 spectrum. Since this screen shot is of the Future Holdings, T-Mobile is will control this spectrum in the future.

Future:

The screen shot below is of the San Diego County Current Holdings. (att) in the PCS B6 column indicates that AT&T is the current operator of the B6 channel.

Current:

For Sacramento (Placer, Sacramento, and Yolo Counties), we can see that AT&T will be the future operator of the PCS B11 channel and that T-Mobile will be the carrier giving up the PCS B11 channel.

Future:

Current:

My last example is in Tucson, AZ. From the National Carriers Report we can see that T-Mobile is increasing their held spectrum by 10MHz.

From the Web Spectrum Viewer, it is clear that T-Mobile is receiving the PCS A10 and A11 channels from Commnet (cmm).

Future:

Current:

Today, we have released Allnet's Insights' March 2017 Mobile Carrier - Spectrum Ownership Analysis Tool. Below are the transactions that have been updated by the FCC from February 1st to February 28th and are included in our update.

The details for all of the below transactions are available by subscribing to Allnet Insights' Web Tool - Basic Module. Our Web Tool provides spectrum transaction detail, a spectrum grid of spectrum owners at a county level, and spectrum database covering all mobile carrier frequencies from 600MHz to 2.5 GHz.

Granted Assignments (Assigning Ownership from Assignor to Assignee):

Granted Leases (Leased to Assignee from Assignor):

New Pending Assignments (Assigning Ownership from Assignor to Assignee):

Pending Leases (Leased to Assignee from Assignor):

Today, we have released Allnet's Insights' February 2017 Mobile Carrier - Spectrum Ownership Analysis Tool. Below are the transactions that have been updated by the FCC from January 1 to January 31 and are included in our update.

The details for all of the below transactions are available by subscribing to Allnet Insights' Web Tool - Basic Module. Our Web Tool provides spectrum transaction detail, a spectrum grid of spectrum owners at a county level, and spectrum database covering all mobile carrier frequencies from 700MHz to 2.5 GHz.

Granted Assignments (Assigning Ownership from Assignor to Assignee):

Granted Leases (Leased to Assignee from Assignor):

New Pending Assignments (Assigning Ownership from Assignor to Assignee):

Pending Leases (Leased to Assignee from Assignor):

Today, we have released Allnet's Insights' January 2017 Mobile Carrier - Spectrum Ownership Analysis Tool. Below are the transactions that have been updated by the FCC from December 1 to December 31 and are included in our update.

The details for all of the below transactions are available by subscribing to Allnet Insights' Web Tool - Basic Module. Our Web Tool provides spectrum transaction detail, a spectrum grid of spectrum owners at a county level, and spectrum database covering all mobile carrier frequencies from 700MHz to 2.5 GHz.

Granted Assignments (Assigning Ownership from Assignor to Assignee):

Granted Leases (Leased to Assignee from Assignor):

New Pending Assignments (Assigning Ownership from Assignor to Assignee):

Pending Leases (Leased to Assignee from Assignor):

In an earlier post, I discussed the ability for Sprint to utilize the Mid-Band Segment of their 2.5GHz spectrum band for LTE. Previously, I had compiled from FCC filings, the BTA markets where video (the original service licensed in the 2.5 GHz band) is still operating. Since the April 2016 post, Allnet Insights' has investigated below the BTA market level to determine the specific licenses that are still broadcasting video. This can be seen in Allnet Insights' Web Spectrum Viewer, in the Spectrum Grid menu.

In the Web Spectrum Viewer, we use the MVU code instead of a typical carrier code (e.g. VZW, SPR, TMO, or ATT) to designate the licenses that are still broadcasting video. In the Los Angeles CMA market, video is operating on all of the mid-band channels (A4, B4, C4, D4, F4, and E4) for both Los Angeles county, and Orange county. Sprint can utilize the entire MBS for LTE in the Riverside and San Bernardino counties.

Los Angeles CMA:

In the Chicago CMA the G4 channel is used in all 6 counties and the E4 channel is used for video in 3 counties.

Chicago CMA:

In the New York CMA, the D4 channel and G4 channel are available for LTE deployment across all but one county in the New York CMA, but the other channels are largely unavailable in the New York CMA.

New York CMA:

What is important to Sprint is the size of the LTE channel or channels that they can create using the Mid-band channels. Using the data from Allnet Insights' Spectrum Grid, we total the number of contiguous channels, rounding to the 3GPP LTE channel sizes of 5, 10, 15, and 20 MHz. The map below displays the total MHz of the LTE channels that Sprint can create in the Mid-band for each county.

For this edition of "How Does Our Data Compare?" we are illustrating how our data compares to a Spectrum Chart that Sprint shared with Fierce Wireless at CTIA 2016. What Sprint is illustrating each of the national carriers average spectrum holdings in each in each frequency band.

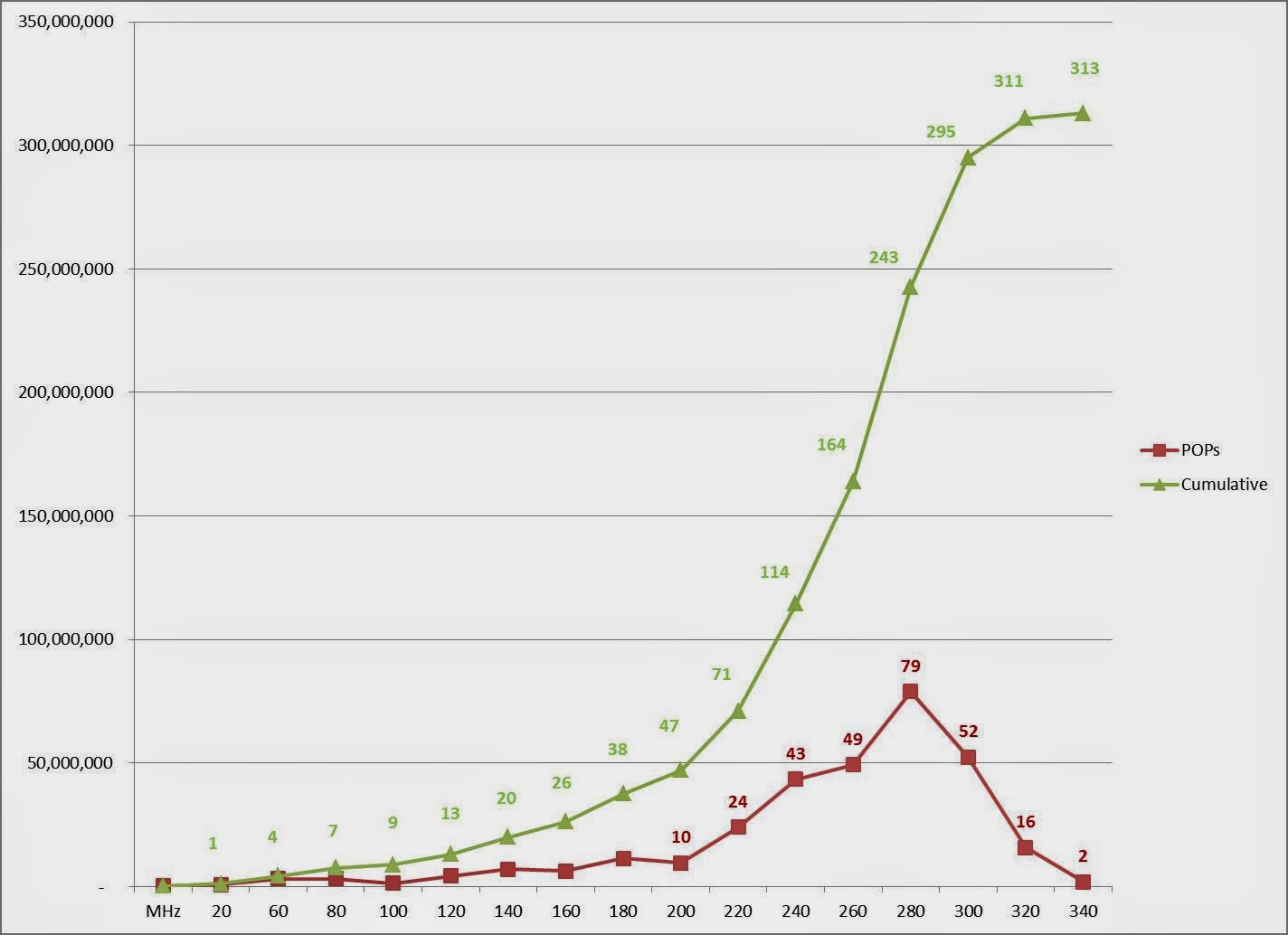

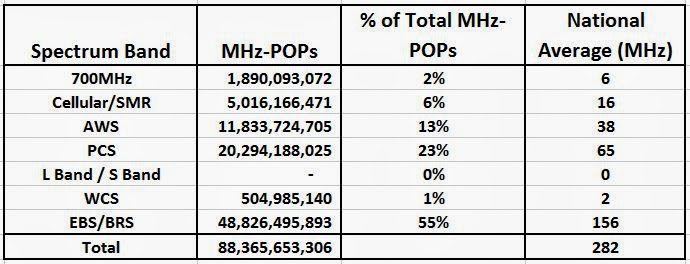

We arrive at the Nationwide average by applying a population-weighted average to our spectrum data that is aggregated at a county-level. As you can see, we hit each carriers spectrum depth exactly except for Sprint's EBS/BRS data which we only miss by 2 MHz. With our October 2016 Version of our Mobile Carrier - Spectrum Ownership Analysis Tool, we are including the ability to chart eight carriers, detailing the average spectrum holdings either by Frequency Band or Band Classification. You can conduct side by side analysis for nearly 1900 US Wireless Carriers. In the chart below you can see the National Averages for spectrum held by the FCC. This total details the AWS-3 and 600 MHz spectrum that will be auctioned by the FCC.

Our National Spectrum by Band Classification chart combines the values for each of the frequency bands into the Low, Mid, or High Band Classifications.

In addition to the National Spectrum values and charts, Allnet's Mobile Carrier - Spectrum Ownership Analysis Tool provides market-level (CMA, EA, PEA), state-level, and county-level reports for 8 carriers side by side.

For this issue of “How does our data compare?” we will look at the following statement from Joan Marsh’s blog. Joan is AT&T's Vice President of Federal Regulatory.

"For AT&T, the restrictions will predominantly impact our ability to compete for spectrum in urban areas. Indeed, our preliminary analysis suggests that we will be restricted in all Top 50 markets except six (Cleveland, Phoenix, Virginia Beach, Charlotte, Raleigh and Greenville to be exact). The restrictions will therefore directly impact our ability to serve customers in the most data hungry markets like NY, Los Angeles, Chicago, San Francisco, Baltimore-DC, Philadelphia, Boston and Dallas."

T-Mobile’s Magenta Herring – Posted by Joan Marsh (AT&T)

Using Allnet Insights’ Spectrum Ownership Analysis Tool we are able to evaluate AT&T’s low band spectrum ownership for all US Partial Economic Area (PEA) market. For this evaluation, we want to see the markets where AT&T’s low band spectrum ownership is less than 45MHz. This would be a PEA market where AT&T would not expect restrictions in the Broadband Incentive Auction (600MHz).

For the Top 50 markets we have the same markets that Joan Marsh indicated in her blog. Also included in the screenshot is amount of low band spectrum that AT&T controls as well as its competitor’s spectrum holdings in the same markets. It is interesting to note that Verizon would be restricted in each of these 6 markets, and T-Mobile only has low band spectrum in 1 of these markets. In addition, we detail how the low band spectrum is divided between cellular spectrum and 700 MHz spectrum.

As we have demonstrated, our data provides similar results to AT&T’s analysis, but it also allows the other national wireless carriers (and over 600 smaller carriers) to be evaluated in the same manner.

Allnet Insights’ Spectrum Ownership Analysis Tool provides county-level spectrum depth and LTE channel configurations, as well as Partial Economic Area (PEA), Economic Area (EA), and Cellular Market Area (CMA) market level spectrum depth evaluations.

Many have grown accustomed to using the FCC Spectrum Dashboard for quick and relatively simple access to spectrum ownership data. This was never a complete solution for spectrum ownership analysis because many frequency blocks (AWS-H, AWS-3, and AWS-4) were never available for query. There have been several blocks of data that have entirely disappeared (700MHz – D block) or been so reduced in quantity that what is left is highly questionable.

Recently, I went to the FCC Spectrum Dashboard to download a large block of spectrum data for analysis. To receive a large data file, the FCC has historically sent a link to a user input email address where the data can be downloaded. After 3 unsuccessful attempts, to receive the email links, I called the FCC support line and was informed that feature was indeed broken and would not be fixed. The customer support representative also indicated that the data available on the site had not been updated since 7/7/2014, over a year ago.

I think we can declare the FCC Spectrum Dashboard dead as a spectrum ownership tool. Since Allnet Insights tracks all spectrum transactions related to the mobile carrier frequencies, we know that since July 9, 2014 over 350 applications have been submitted changing the ownership or leasing on nearly 700 call signs. These numbers don’t include any of new AWS-3 call signs which include an additional 1,614 call signs. In all, the FCC Spectrum Dashboard has incorrect data for nearly 2000 call signs.

Fortunately, AllNet Insights’ Spectrum Owners Analysis Tool and its National Carrier reports continue to provide the industry leading information on spectrum ownership through our carefully managed spectrum ownership database This database maintains the current licensee, lease, and future licensee for every block of US wireless carrier spectrum.

|

| FCC 12-148A1 - Figure 2 |