Free Shipping On world wide

- HOME

- PRODUCTS

- IN THE NEWS

- SPECTRUM BLOG

- WEB SPECTRUM VIEWER

-

English

-

USD

Free Shipping On world wide

Recently in our spectrum transaction tracking we discovered some Millimeter Wave Special Temporary Authority (STA) licenses that AT&T and Verizon have filed in the 39GHz band to conduct wideband testing and for AT&T it appears the spectrum will be used for a market launch later this year.

To see what is going on, let's look at Verizon and AT&T's ownership of the 39GHz band in the Chicago PEA market (PEA003) with our Spectrum Grid module. The Spectrum Grid modules is one of nineteen analysis modules in our Millimeter Wave - Spectrum Ownership Analysis Tool. Below you can see the specific channels that AT&T and Verizon control. This spectrum is still paired, meaning the lower channels are for uplink and the upper channels are for downlink. It is apparent that Verizon and AT&T's channels are commingled and that neither carrier can utilize a channel larger than 150MHz (AT&T is limited to 50MHz). You can see 4 channels that the FCC does control in the lower band, but these are not the channels that AT&T or Verizon requested in their STA.

They each requested channels in the new 37GHz band which will be auctioned later this year. This spectrum is adjacent to the existing 39GHz licensed bands

The spectrum allocations that Verizon and AT&T have requested in Chicago are indicated below.

This allocation provides both AT&T and Verizon with 400MHz for wideband 5G. For AT&T, this is likely the spectrum they will utilize for the Chicago market launch announced for later this year. Verizon likely launched their 5G UWB network using the 28GHz L1 and L2 spectrum seen below, so this 37GHz allotment is likely for network testing.

We have highlighted the effect of the temporary licenses in the Chicago (PEA003). We noted that AT&T has also requested STA licenses in Raleigh (PEA045), Oklahoma City (PEA039), Charlotte (PEA043) and Philadelphia (PEA006). Verizon requested STA licenses in New York (PEA001), Cleveland (PEA014), Cincinnati (PEA025), and Tallahassee (PEA072)

On March 21st, the FCC released a Notice of Procedures describing how existing 39GHz spectrum ownership below will be remapped to the new 39GHz configuration. We thought it would be beneficial to see how the FCC arrived at their results.

Current Configuration:

Future Configuration:

The procedures the FCC announced will provide a route for the existing 39GHz owners to essentially trade-in their spectrum for vouchers that can be used in Auction 103. The FCC published a summary of the aggregated holdings data for each of the 39GHz licensees so we decided to use the data from our Millimeter Wave - Spectrum Ownership Analysis Tool to show the underlying calculations.

We are able to use the data from our Millimeter Wave - Spectrum Ownership Analysis Tool to determine the aggregate MHz-POPs value for PEA003 (Chicago). To find the aggregate MHz-POPs we must first find the MHz-POPs contribution for each of AT&T's licenses (call signs) in the Chicago market. Below are each of the county MHz-POPs components for each call sign. We have indicated whether the license covers the entire county or whether it is a partial license in the Full/Partial County column. The county MHz-POPs component is found by multiplying the bandwidth for each call sign by the county population. The total aggregate MHz-POPs is the sum of the county MHz-POPs for all of AT&T's licenses. Using this process, we have found AT&T's aggregate MHz-POPs to by 2,817,188,800 compared to the FCC's results of 2,815,434,000.

| Market | CallSign | Channel Block | Full/Partial County | State | County | Bandwidth | County Population | MHz-POPs |

| PEA003 | WRBI252 | 1A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 |

| Chicago | DuPage County | 50 | 916,924 | 45,846,200 | ||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI253 | 1B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI590 | 4A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBI591 | 4B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBJ298 | 8A | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBJ299 | 8B | Full | IL | Cook County | 50 | 5,194,675 | 259,733,750 | |

| DuPage County | 50 | 916,924 | 45,846,200 | |||||

| Grundy County | 50 | 50,063 | 2,503,150 | |||||

| Kane County | 50 | 515,269 | 25,763,450 | |||||

| Kankakee County | 50 | 113,449 | 5,672,450 | |||||

| Kendall County | 50 | 114,736 | 5,736,800 | |||||

| Lake County | 50 | 703,462 | 35,173,100 | |||||

| McHenry County | 50 | 308,760 | 15,438,000 | |||||

| Will County | 50 | 677,560 | 33,878,000 | |||||

| IN | Lake County | 50 | 496,005 | 24,800,250 | ||||

| LaPorte County | 50 | 111,467 | 5,573,350 | |||||

| Porter County | 50 | 164,343 | 8,217,150 | |||||

| WRBK275 | 13A | Partial | IL | Kane County | 50 | 21,235 | 1,061,750 | |

| Kendall County | 50 | 13,076 | 653,800 | |||||

| McHenry County | 50 | 37,438 | 1,871,900 | |||||

| 13B | Partial | IL | Kane County | 50 | 21,235 | 1,061,750 | ||

| Kendall County | 50 | 13,076 | 653,800 | |||||

| McHenry County | 50 | 37,438 | 1,871,900 | |||||

| 2,817,188,800 |

The Market MHz-POPs value is found by multiplying the new 39GHz channel size (100MHz) by the total population of the Chicago PEA.

| Market | Bandwidth | PEA Population | Market MHz-POPs |

| PEA003 (Chicago) | 100 | 9,366,713 | 936,671,300 |

The next calculation provides the number of blocks that AT&T is authorized to receive in the 39GHz auction by relinquishing their current licenses. Our analysis indicates that AT&T will start with slightly more than 3 - 100MHz channel blocks in Chicago before the auction starts.

| Market | Aggregate MHz-POPs | Market MHz-POPs | Channel Blocks |

| PEA003 (Chicago) | 2,817,188,800 | 936,671,300 | 3.00766 |

Two questions for all of the wireless network installers and drive testers:

1) Where can you get the spectrum assignments for all of the mobile carrier bands with in a county?

2) How can you determine if the licensed spectrum assignment will change in the near future?

Allnet Insights' Web Spectrum Viewer now includes a Wireless Survey which details the wireless carrier that currently controls each block of Mobile Carrier spectrum (600MHz-2.5GHz) for a selected US county. In addition, the Wireless Survey indicates whether there are any filed transaction that will move that spectrum to another wireless carrier, as indicated in the Future column.

The output table details the spectrum assignment's,licensees, and bandwidth for each block and is sorted from lowest frequency to highest frequency. This output table can be exported as a .csv file.

| Purpose | Assignee | Assignor | CallSign | Map | RadioService | Market | ChannelBlock |

| New Lease | Cimaron Telephone | Cross Telephone Company | WRBQ838 | AWS3 | CMA598 - Oklahoma 3 - Grant | G | |

| New Lease | GE MDS LLC | Access 700 | WPRR314 | 700MHz GB | MEA025 - Nashville | A | |

| New Lease | GE MDS LLC | Access 700 | WPRV427 | 700MHz GB | MEA008 - Atlanta | A | |

| New Lease | GE MDS LLC | Access 700 | WPRV430 | 700MHz GB | MEA024 - Birmingham | A | |

| New Lease | GE MDS LLC | Access 700 | WPRV439 | 700MHz GB | MEA038 - San Antonio | A | |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | BRS1 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | E4 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | F1 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | F2 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | F3 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | F4 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | H1 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | H2 |

| New Lease | SpeedConnect | Sprint | B064 | Map | BRS | BTA064 - Butte, MT | H3 |

| New Lease | SpeedConnect | Sprint | B144 | Map | BRS | BTA144 - Flagstaff, AZ | BRS1 |

| New Lease | SpeedConnect | Sprint | B144 | Map | BRS | BTA144 - Flagstaff, AZ | E4 |

| New Lease | SpeedConnect | Sprint | B144 | Map | BRS | BTA144 - Flagstaff, AZ | F4 |

| New Lease | SpeedConnect | Sprint | B167 | Map | BRS | BTA167 - Grand Island-Kearney, NE | BRS1 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | BRS2 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | E1 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | E2 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | E3 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | E4 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | F1 |

| New Lease | SpeedConnect | Sprint | B171 | Map | BRS | BTA171 - Great Falls, MT | F4 |

| New Lease | SpeedConnect | Sprint | B202 | Map | BRS | BTA202 - Idaho Falls, ID | BRS1 |

| New Lease | SpeedConnect | Sprint | B202 | Map | BRS | BTA202 - Idaho Falls, ID | BRS2 |

| New Lease | SpeedConnect | Sprint | B202 | Map | BRS | BTA202 - Idaho Falls, ID | E4 |

| New Lease | SpeedConnect | Sprint | B202 | Map | BRS | BTA202 - Idaho Falls, ID | F4 |

| New Lease | SpeedConnect | Sprint | B205 | Map | BRS | BTA205 - Iowa City, IA | BRS1 |

| New Lease | SpeedConnect | Sprint | B205 | Map | BRS | BTA205 - Iowa City, IA | BRS2 |

| New Lease | SpeedConnect | Sprint | B205 | Map | BRS | BTA205 - Iowa City, IA | E4 |

| New Lease | SpeedConnect | Sprint | B205 | Map | BRS | BTA205 - Iowa City, IA | F4 |

| New Lease | SpeedConnect | Sprint | B300 | Map | BRS | BTA300 - Missoula, MT | BRS1 |

| New Lease | SpeedConnect | Sprint | B353 | Map | BRS | BTA353 - Pocatello, ID | BRS1 |

| New Lease | SpeedConnect | Sprint | B353 | Map | BRS | BTA353 - Pocatello, ID | BRS2 |

| New Lease | SpeedConnect | Sprint | B353 | Map | BRS | BTA353 - Pocatello, ID | E4 |

| New Lease | SpeedConnect | Sprint | B353 | Map | BRS | BTA353 - Pocatello, ID | F4 |

| New Lease | SpeedConnect | Sprint | B422 | Map | BRS | BTA422 - Sioux Falls, SD | BRS1 |

| New Lease | SpeedConnect | Sprint | B422 | Map | BRS | BTA422 - Sioux Falls, SD | BRS2 |

| New Lease | SpeedConnect | Sprint | B422 | Map | BRS | BTA422 - Sioux Falls, SD | E4 |

| New Lease | SpeedConnect | Sprint | B422 | Map | BRS | BTA422 - Sioux Falls, SD | F4 |

| New Lease | SpeedConnect | Sprint | B451 | Map | BRS | BTA451 - Twin Falls, ID | BRS1 |

| New Lease | SpeedConnect | Sprint | B451 | Map | BRS | BTA451 - Twin Falls, ID | E4 |

| New Lease | SpeedConnect | Sprint | B451 | Map | BRS | BTA451 - Twin Falls, ID | F4 |

| New Lease | SpeedConnect | Sprint | WFY431 | Map | BRS | P00089 - P35 GSA,40-43-38 N,99-7-41.3 W | BRS1 |

| New Lease | SpeedConnect | Sprint | WFY595 | Map | BRS | P03002 - P35 GSA,41-32-48.1 N,90-27-56.5 W | BRS1 |

| New Lease | SpeedConnect | Sprint | WGW275 | Map | BRS | P03471 - P35 GSA,43-28-24.1 N,83-50-39.9 W | E4 |

| New Lease | SpeedConnect | Sprint | WHI959 | Map | BRS | P00168 - P35 GSA,43-59-30.9 N,96-46-11.2 W | F4 |

| New Lease | SpeedConnect | Sprint | WHT588 | Map | BRS | P03685 - P35 GSA,41-31-58.1 N,90-34-40.5 W | E4 |

| New Lease | SpeedConnect | Sprint | WLK328 | Map | BRS | P01359 - P35 GSA,43-14-38 N,97-22-39.2 W | F4 |

| New Lease | SpeedConnect | Sprint | WLK384 | Map | BRS | P01362 - P35 GSA,43-14-38 N,97-22-39.2 W | E4 |

| New Lease | SpeedConnect | Sprint | WLW827 | Map | BRS | P01384 - P35 GSA,31-25-16.6 N,100-32-37.3 W | F1234 |

| New Lease | SpeedConnect | Sprint | WLW894 | Map | BRS | P01898 - P35 GSA,41-31-58.1 N,90-34-40.5 W | F4 |

| New Lease | SpeedConnect | Sprint | WMH800 | Map | BRS | P02690 - P35 GSA,34-13-58.1 N,112-22-15.6 W | E4 |

| New Lease | SpeedConnect | Sprint | WMI345 | Map | BRS | P01925 - P35 GSA,41-54-33 N,91-39-17.6 W | E4 |

| New Lease | SpeedConnect | Sprint | WMI827 | Map | BRS | P02939 - P35 GSA,34-42-17.1 N,112-6-57.6 W | E4 |

| New Lease | SpeedConnect | Sprint | WMI864 | Map | BRS | P02941 - P35 GSA,34-42-17.1 N,112-6-57.6 W | F4 |

| New Lease | SpeedConnect | Sprint | WML478 | Map | BRS | P03544 - P35 GSA,31-25-16.6 N,100-32-37.3 W | BRS1 |

| New Lease | SpeedConnect | Sprint | WMX344 | Map | BRS | P03719 - P35 GSA,43-30-10.9 N,96-34-39.2 W | F4 |

| New Lease | SpeedConnect | Sprint | WMX358 | Map | BRS | P01947 - P35 GSA,43-30-10.9 N,96-34-39.2 W | E4 |

| New Lease | SpeedConnect | Sprint | WMX656 | Map | EBS | P00155 - P35 GSA,42-43-54 N,114-25-7 W | D1234 |

| New Lease | SpeedConnect | Sprint | WMX678 | Map | EBS | P00017 - P35 GSA,42-43-54 N,114-25-7 W | C1234 |

| New Lease | SpeedConnect | Sprint | WMX908 | Map | BRS | P03551 - P35 GSA,31-25-16.6 N,100-32-37.3 W | E1234 |

| New Lease | SpeedConnect | Sprint | WNTC543 | Map | BRS | P01566 - P35 GSA,31-25-16.6 N,100-32-37.3 W | H1 |

| New Lease | SpeedConnect | Sprint | WNTC543 | Map | BRS | P01566 - P35 GSA,31-25-16.6 N,100-32-37.3 W | H2 |

| New Lease | SpeedConnect | Sprint | WQLW472 | Map | BRS | BTA070 - Cedar Rapids, IA | BRS2 |

| New Lease | SpeedConnect | Sprint | WQLW472 | Map | BRS | BTA070 - Cedar Rapids, IA | E4 |

| New Lease | SpeedConnect | Sprint | WQLW472 | Map | BRS | BTA070 - Cedar Rapids, IA | F4 |

| New Lease | SpeedConnect | Sprint | WQLW474 | Map | BRS | BTA105 - Davenport, IA-Moline, IL | BRS2 |

| New Lease | SpeedConnect | Sprint | WLW970 | Map | BRS | P02673 - P35 GSA,35-14-2 N,111-36-27.6 W | F4 |

| New Lease | SpeedConnect | Sprint | WMI320 | Map | BRS | P02694 - P35 GSA,35-14-29 N,111-36-37.6 W | E4 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | BRS1 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | E4 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | F1 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | F2 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | F3 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | F4 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | H1 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | H2 |

| New Lease | SpeedConnect | Sprint | B011 | Map | BRS | BTA011 - Alpena, MI | H3 |

| New Lease | SpeedConnect | Sprint | B307 | Map | BRS | BTA307 - Mt. Pleasant, MI | E4 |

| New Lease | SpeedConnect | Sprint | B307 | Map | BRS | BTA307 - Mt. Pleasant, MI | F4 |

| New Lease | SpeedConnect | Sprint | B390 | Map | BRS | BTA390 - Saginaw-Bay City, MI | E4 |

| New Lease | SpeedConnect | Sprint | B390 | Map | BRS | BTA390 - Saginaw-Bay City, MI | F4 |

| New Lease | T-Mobile | RigNet | WPWV330 | 700MHz | CMA306 - Gulf of Mexico | C |

In our last post we were discussing the next steps for the US millimeter wave spectrum after FiberTower and the FCC settled FiberTower's licensing issues. As we prepare for a 28GHz auction in November, and a 24GHz auction early next year, let's take a look at how each of the new millimeter wave frequency bands are configured. Each of these images is taken from our updated Millimeter Wave - Spectrum Ownership Analysis Tool which is now reflecting the new channel band plans for 24GHz, 37GHz, and 47GHz.

24 GHz Spectrum:

In this view we show both the expanded 24GHz band configuration and the old 24GHz configuration. All of the spectrum depth values are calculated from the New 24GHz data. We have left the old 24GHz configuration, so you can continue to see the remaining 24GHz spectrum licenses which will need to be moved over to the New 24GHz by the FCC. The current licenses are licensed for a 40MHz uplink and 40MHz downlink which won't map properly to the new band plan.

37GHz Spectrum:

For the 37/39GHz bands we show the new 37GHz band alongside the reconfigured 39GHz band. The new 39GHz columns are not populated because the existing spectrum holders will need to be transitioned to the larger/unpaired channels in the new 39GHz plan. We are providing spectrum depth values for the new 37GHz spectrum and the old 39GHz spectrum.

47GHz Spectrum:

We have added the new 47GHz band configurations to the Spectrum Grid and each of the spectrum depth modules.

PEA Market Analysis:

Our last addition, is a PEA Market Analysis module. This module displays spectrum depths for each selected carrier using the new FCC Auction market structure. For the 28GHz auction, you can see the amount of spectrum that will be available in each of the PEAs in the LMDS A (FCC) column on the far right of the chart.

Yesterday Allnet Insights & Analytics presented at the Wells Fargo 5G forum. Below are several of the slides that describe the millimeter wave spectrum holdings for each of the parties involved in the current millimeter wave deals. Each of these slides is a direct analysis output from our Millimeter Wave - Spectrum Ownership Analysis Tool. In these slides we have selected 8 carriers from the 173 carriers available in the tool. The first slide compares the National Weighted Average spectrum depth for each of the carriers. Verizon's spectrum position is displayed as NextLink Wireless since Verizon at the time this slide was created was only leasing NextLink's spectrum. In this set of slides we also highlight the risk surrounding the FiberTower transaction for AT&T. The largest portion of the FiberTower transaction is for licenses that the FCC has terminated. It is unknown how many of these licenses will be restored and added to AT&T's spectrum holdings.

While the National Average slide highlights how much spectrum each carrier has on average across the county, networks are deployed using the available spectrum within a market. The slides below highlight the amount of spectrum that each carrier has in a CMA (Cellular Market Area). The Top 5 markets are in the first slide including Los Angeles, New York, Chicago, Dallas and Houston.

The remaining Top 10 markets are in the second slide: Philadelphia, Washington D.C., Detroit, Atlanta, and Boston.

The last slide highlights the estimated MHz-POPs for each of the carriers for their Millimeter Wave spectrum. It is worth noting that the ranges for Mobile Carrier spectrum (600MHz-2.5GHz) for the National Carriers is 30B MHz-POPs to 65B MHz-POPs. On this chart, the lowest range is 50B MHz-POPs.

In my most recent post on the filed FCC Transactions for February 2017 there were over 275 call signs that were assigned to new licensees and nearly 100 call signs that were leased. In an industry driven by spectrum, these changes affect the operations for every wireless carrier, they change site interference, and they affect the channels that are programmed into private repeaters and DAS systems.

So how can your company stay on top of the changes that may affect your markets. Allnet Insights' publishes a National Carrier Spectrum Depth Report which details the spectrum held by Verizon, AT&T, T-Mobile, Sprint, Dish, and USCellular in the Top 100 Cellular Market Areas (CMA). We report both the spectrum that each carrier currently holds (Current Holdings) and the spectrum they will hold in the future (Future Holdings) based on pending FCC transactions. Reporting on both current and future holdings enables Allnet Insights' to also report on the changes between current and future holdings which highlight the location and quantity of spectrum that is changing hands.

Below is a screenshot of the 11th through the 25th most populated CMA markets in our February 2017 report. This highlights the markets where the national carriers are either increasing or decreasing their spectrum holdings. In the Excel report you can reveal specific holdings by frequency bands that are changing but for this post, we will stay with the total spectrum view. From this view, you can see that in San Diego, T-Mobile is increasing their held spectrum by 5MHz while AT&T is decreasing their held spectrum by 5MHz. The reverse is happening in the Sacramento CMA.

We also highlight the spectrum that is changing hands in our Web Spectrum Viewer. In the Spectrum Grid menu, we lower case the 3 letter carrier code to indicate that the carrier ownership is changing from the current to the future. Looking at the same San Diego market (San Diego County) you can see (tmo) on the PCS B6 spectrum. Since this screen shot is of the Future Holdings, T-Mobile is will control this spectrum in the future.

Future:

The screen shot below is of the San Diego County Current Holdings. (att) in the PCS B6 column indicates that AT&T is the current operator of the B6 channel.

Current:

For Sacramento (Placer, Sacramento, and Yolo Counties), we can see that AT&T will be the future operator of the PCS B11 channel and that T-Mobile will be the carrier giving up the PCS B11 channel.

Future:

Current:

My last example is in Tucson, AZ. From the National Carriers Report we can see that T-Mobile is increasing their held spectrum by 10MHz.

From the Web Spectrum Viewer, it is clear that T-Mobile is receiving the PCS A10 and A11 channels from Commnet (cmm).

Future:

Current:

Today, we have released Allnet's Insights' March 2017 Mobile Carrier - Spectrum Ownership Analysis Tool. Below are the transactions that have been updated by the FCC from February 1st to February 28th and are included in our update.

The details for all of the below transactions are available by subscribing to Allnet Insights' Web Tool - Basic Module. Our Web Tool provides spectrum transaction detail, a spectrum grid of spectrum owners at a county level, and spectrum database covering all mobile carrier frequencies from 600MHz to 2.5 GHz.

Granted Assignments (Assigning Ownership from Assignor to Assignee):

Granted Leases (Leased to Assignee from Assignor):

New Pending Assignments (Assigning Ownership from Assignor to Assignee):

Pending Leases (Leased to Assignee from Assignor):

Today, we have released Allnet's Insights' January 2017 Mobile Carrier - Spectrum Ownership Analysis Tool. Below are the transactions that have been updated by the FCC from December 1 to December 31 and are included in our update.

The details for all of the below transactions are available by subscribing to Allnet Insights' Web Tool - Basic Module. Our Web Tool provides spectrum transaction detail, a spectrum grid of spectrum owners at a county level, and spectrum database covering all mobile carrier frequencies from 700MHz to 2.5 GHz.

Granted Assignments (Assigning Ownership from Assignor to Assignee):

Granted Leases (Leased to Assignee from Assignor):

New Pending Assignments (Assigning Ownership from Assignor to Assignee):

Pending Leases (Leased to Assignee from Assignor):

With this blog post, we are highlighting the Change in Spectrum Holdings feature of our National Carriers - Spectrum Holdings reports. In this report, we detail the spectrum holdings for each of the national carriers, including Dish, and USCellular. The first segment of the report details each carrier's future holdings, tracking the effects of all pending FCC transactions. The second segment of the report details each carrier's current spectrum holdings. Using each of these segments, we provide a Change in Spectrum Holdings segment which highlights the CMA markets where a carrier's spectrum holding are increasing (+) or decreasing (-) because of filed FCC transactions.

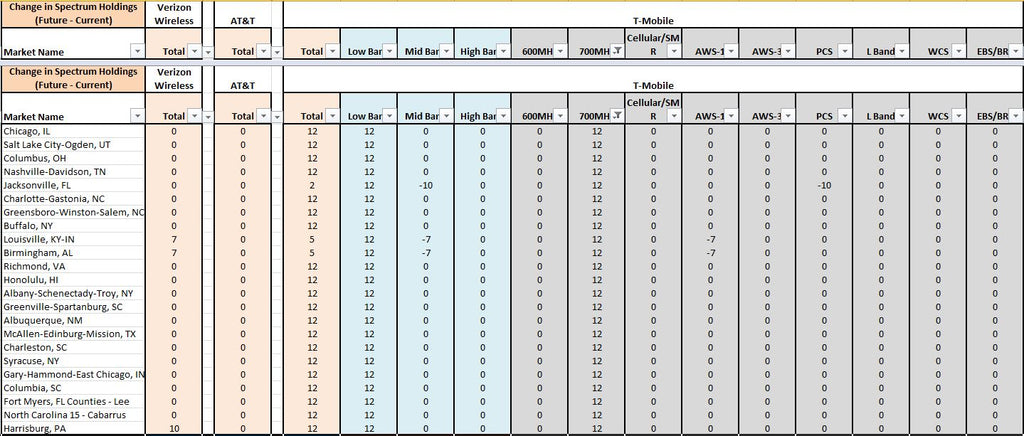

In the view above, from August 2016, you can see the summary details for the spectrum additions and subtractions for each of the national wireless carriers. This view highlights a spectrum trade between Sprint and T-Mobile in the Cleveland market (5 MHz) as well as the T-Mobile's pending 700MHz A-Block transactions.

The view above details the band classifications (low, mid, or high) and the frequency band that contribute to T-Mobile's 12 MHz increase in spectrum. The August 2016 report concludes that the transactions for all of the listed market names are still pending.

Now looking at the September 2016, the Allnet's Spectrum Ownership Analysis Tool has updated the transactions that were consummated during August 2016. The only pending 700MHz - A Block transaction is T-Mobile's purchase of Laser in Chicago, IL.

For the cost of a monthly subscription to the National Carrier - Spectrum Depth Reports ($495/mo), the monthly effect of pending and closed transaction can be seen and evaluated.

For this edition of "How Does Our Data Compare?" we are illustrating how our data compares to a Spectrum Chart that Sprint shared with Fierce Wireless at CTIA 2016. What Sprint is illustrating each of the national carriers average spectrum holdings in each in each frequency band.

We arrive at the Nationwide average by applying a population-weighted average to our spectrum data that is aggregated at a county-level. As you can see, we hit each carriers spectrum depth exactly except for Sprint's EBS/BRS data which we only miss by 2 MHz. With our October 2016 Version of our Mobile Carrier - Spectrum Ownership Analysis Tool, we are including the ability to chart eight carriers, detailing the average spectrum holdings either by Frequency Band or Band Classification. You can conduct side by side analysis for nearly 1900 US Wireless Carriers. In the chart below you can see the National Averages for spectrum held by the FCC. This total details the AWS-3 and 600 MHz spectrum that will be auctioned by the FCC.

Our National Spectrum by Band Classification chart combines the values for each of the frequency bands into the Low, Mid, or High Band Classifications.

In addition to the National Spectrum values and charts, Allnet's Mobile Carrier - Spectrum Ownership Analysis Tool provides market-level (CMA, EA, PEA), state-level, and county-level reports for 8 carriers side by side.

For this blog post I am going to use some of the new features of the Millimeter Wave - Spectrum Ownership Analysis Tool, to break down Verizon's agreement to lease XO's Millimeter Wave Spectrum.

First of all, our data source for this analysis is the Future Holdings data which will reflect Verizon's future lease of XO's spectrum. Allnet's CMA Market Analysis Module details Verizon's spectrum holdings for each of the Top 20 CMA markets (below). From this analysis it is easy to see the markets where Verizon will have significant LMDS A (28 GHz) and LMDS B (31 GHz) spectrum. In addition, markets with out spectrum (Phoenix) and the limited markets with 39 GHz spectrum are easily identified.

CMA Market Analysis:

Next we will look at the State & National Analysis Module to determine the average spectrum depth across the Nation or at a State Level. Looking at the National Average Spectrum Depth, we can see that Verizon averages 576 MHz of millimeter wave spectrum with 511 MHz of that being LMDS A spectrum, 53 MHz being LMDS B spectrum and 12 MHz being 39 GHz spectrum.

State & National Analysis Module:

Last we will look at how many MHz-POPs are included and how they are distributed between each of the frequency blocks. Allnet's MHz-POPs Analysis Module clearly details that this transaction would provide Verizon over 180 billion MHz-POPs. 158 billion of those MHz-POPs are from the LMDS A frequency band, 16 billion from the LMDS B frequency band, and nearly 4 billion from the 39 GHz frequency band.

MHz-POPs Analysis Module:

Most wireless carrier assessments are focused on the spectrum depth that each carrier controls. This is typically indicated by the number of MHz that a carrier controls (owns) either in a county or a market. Many evaluations are focused on the total MHz that a carrier owns although our Spectrum Ownership Analysis Tool and National Carrier reports break the spectrum depth down by both frequency band (700, Cellular, PCS, AWS, WCS, and EBS/BRS) as well as low-band, mid-band, and high-band. The band breakdowns are important because different bands have better or worse performance for coverage or in-building penetration. Understanding each carriers strengths or weakness for that criteria is important. In addition, since each carrier's LTE deployments have been targeted in specific frequency bands, the frequency band spectrum depth is an important metric to indicate the potential LTE channel size.

LTE Effective Spectrum is a much better indication of a carrier's usable spectrum depth than straight spectrum depth. LTE Effective Spectrum is the sum of the spectrum used by all of a carrier's potential LTE channels. We calculate each carrier's available LTE channels in our Mobile Carrier - Spectrum Ownership Analysis Tool by evaluating the contiguous spectrum that each carrier has in each frequency band.. In the tool, we detail the available LTE channels within each frequency band, but below we simplify the analysis here by listing only the quantity each channel size (5x5, 10x10,...). These LTE channel counts are provided at a CMA market level. To calculate the Effective LTE Spectrum value each of the channel widths (MHz) are summed. For Verizon in the Los Angeles CMA, four 10x10 channels and one 20x20 channel works out to: 4 x 10 + 4 x 10 + 1 x 20 + 1 x 20 = 120 MHz. Each channel is listed twice to reflect both transmit and receive (FDD) spectrum.

As you compare Verizon's Total Spectrum with their Effective LTE Spectrum at a market level, it is apparent that roughly 6% of Verizon's spectrum is not deployable for LTE. For Verizon, this lost spectrum relates to 2.5 MHz slices of cellular spectrum and 1 MHz slices of 700 MHz spectrum.

As you compare AT&T's Total Spectrum with their Effective LTE Spectrum at a market level, it is apparent that a much larger portion of AT&T's spectrum is not deployable for LTE. AT&T loses between 15% and 22% of there Total Spectrum on a market basis. This lost spectrum primarily relates the WCS spectrum (10MHz) AT&T dedicated as a guard band for satellite audio, along with 2.5 MHz slices of cellular spectrum and 1 MHz slices of 700 MHz spectrum.

As you compare T-Mobile's Total Spectrum with their Effective LTE Spectrum at a market level, it is apparent that very little of T-Mobile's spectrum is not deployable for LTE. T-Mobile typically loses 2% of their Total Spectrum on a market basis. This lost spectrum relates to the 6 MHz channels of 700 MHz spectrum only being used for 5x5 LTE. There are specific markets (San Diego @ 9%) where T-Mobile controls a 12.5 MHz channel which can only be deployed as a 10x10 LTE channel effectively losing ability to use the remaining 2.5 MHz unless a new acquisition would add adjacent spectrum.

We have left the analysis of Sprint's Lost Spectrum for another time because Sprint's combination of TDD and FDD spectrum makes their analysis significantly more complicated.

These charts reflect the Future data set from Allnet Insight's Spectrum Ownership Analysis Tool (February 2016 Version).

How much backhaul capacity do you provide to each cell site for each 10MHz of LTE spectrum?

225 Mbps should be provided for each 10MHz of spectrum (75Mbps per sector)to prevent backhaul from creating a bottleneck.

What percentage of your sites utilize Verizon facilities for backhaul versus alternative backhaul providers?

Verizon has a significant cost advantage in the markets where they provide local telephone service by using internal resources for cell site backhaul.

What is your average monthly backhaul cost per cell site ($/Mbps) for the site using an alternative backhaul provider?

Locations where Verizon utilizes an alternative backhaul provider, the site expense for backhaul will begin to dominate the network cost of service. With the move to data, the site lease (average $1500/mo) is dominated by the backhaul lease ($8000/mo). This becomes more painful as you consider the need for doubling data capacity which could then double your site backhaul expense.

How do you account for the backhaul assets that are provided from your wireline subsidiaries to your wireless business? Are there any charge backs or internal bills based upon usage or capacity?

Now that Verizon has purchased Vodofone’s interest, this is less of an issue. However, concerns still arise that wireline assets are not properly valued for the benefit they provide the wireless business.

Are you deploying RRH (Remote Radio Head) technology? To what percentage of your sites?

Verizon has been the quietest of the national carriers on their plans to deploy RRH technology. It would make sense for Verizon to deploy RRH technology for their AWS and PCS LTE sectors so those sectors can have more similar coverage to their low band (700 MHz) sectors. In markets where Verizon is building an extensive small cell network uses their AWS and PCS frequencies, they will likely not use the RRH technology within the small cell network area.

We are proud to announce the release of our September 2015 Spectrum Ownership Analysis Tool. In this release we have updated our data set to include the following August spectrum transactions among others:

Additionally with the September 2015 Spectrum Ownership Analysis Tool, we have added the Channel Block analysis module. This module will detail spectrum holdings for an individual carrier by individual channels. Previously, we have provided analysis modules which detail spectrum holdings by frequency band (700MHz, SMR/Cellular, PCS, AWS, WCS, and BRS/EBS), by band class (Low Band, Mid Band, and High Band), and by LTE band (Band 12, Band 17, Band 5) The new Channel Block analysis module provides the reader with a clear understand of what spectrum is held in a county. This is organized by specific colored channel block.

These graphs detail the peak capacity for downlink files and streaming video for the four major national wireless carriers plus Dish and USCellular. They illustrate the peak capacity on a market-by-market basis. In creating the graphs, I anticipate the usage of each wireless carrier’s total spectrum available, not just the spectrum they have dedicated to LTE at this time. These graphs allow you to see the significant capacity advantage that Sprint will have once they deploy their 2.5GHz spectrum. They also provide a market-by-market comparison of AT&T and Verizon capacity. You can see that AT&T has a capacity advantage versus Verizon in all Top 20 markets except Minneapolis-St. Paul. In addition, you can see the relatively low capacity that T-Mobile is able to offer and the capacity that Dish could provide after they launch a network.

I was able to construct these graphs by using Allnet Insights and Analytics Spectrum Ownership Analysis Tool determine the number of LTE channels that each carrier’s spectrum can support.

Assuming that each LTE channel had the follow achievable LTE Peak Data Rates:

These rates were applied to each of the carriers LTE channels to create a total peak downlink throughput. For all EBS/BRS spectrum (Sprint’s 2.5GHz spectrum), I assumed TDD (Time Division Duplex) LTE operation and each channel’s throughput was reduced to 75% to reflect the 75:25 downlink to uplink ratio for TDD operation. TDD LTE utilizes a single radio channel to both transmit to the mobile device (downlink) and transmit from the mobile device (uplink). In TDD LTE timeslots, similar to the wedges on the Wheel of Fortune, carry either downlink traffic or uplink traffic during that time interval. Since internet traffic is typically 75% downlink and 25% uplink, US operators dedicate 75% of the wedges to downlink and 25% to uplink. Most US spectrum bands are configured for FDD (Frequency Division Duplex) LTE, which utilizes two radio channels, one to transmit to the mobile device (downlink), and one to transmit from the mobile device (uplink).

For this issue of “How does our data compare?” we will look at the following statement from Andy Levin’s blog. Andy is T-Moble’s Senior Vice President of Government Affairs.

"AT&T’s practice of making promises it cannot keep is matched only by its ability to make claims that cannot withstand scrutiny. In the run-up to the 600 MHz auction, for instance, AT&T has derided the spectrum reserve as a “set aside” that “picks winners and losers.”

The claim is laughable: if the reserve is a set-aside, it is a set-aside that AT&T or Verizon can claim in nearly three-quarters of the country. The map below shows the markets where AT&T or Verizon can purchase all the spectrum blocks available in the upcoming 600 MHz auction."

AT&T Plays a Broken Record of Broken Promises – Andy Levin, T-Mobile, Sr VP, Government Affairs

Using Allnet Insights’ Spectrum Ownership Analysis Tool we are able to evaluate AT&T and Verizon’s low band spectrum ownership for all US Partial Economic Area (PEA) markets. We then created a geographic map. This map graphed 4 categories:

The purple areas from Allnet Insights’ map match the white areas from T-Mobile’s map with the exception of a rural PEA in northern Montana. These areas represent the PEA markets that both AT&T and Verizon will be limited in the ability to acquire addition low band spectrum. Clearly from Allnet Insights’ map you can see that there are many additional markets where either AT&T or Verizon is limited, but not both.

For this issue of “How does our data compare?” we will look at the following statement from Joan Marsh’s blog. Joan is AT&T's Vice President of Federal Regulatory.

"For AT&T, the restrictions will predominantly impact our ability to compete for spectrum in urban areas. Indeed, our preliminary analysis suggests that we will be restricted in all Top 50 markets except six (Cleveland, Phoenix, Virginia Beach, Charlotte, Raleigh and Greenville to be exact). The restrictions will therefore directly impact our ability to serve customers in the most data hungry markets like NY, Los Angeles, Chicago, San Francisco, Baltimore-DC, Philadelphia, Boston and Dallas."

T-Mobile’s Magenta Herring – Posted by Joan Marsh (AT&T)

Using Allnet Insights’ Spectrum Ownership Analysis Tool we are able to evaluate AT&T’s low band spectrum ownership for all US Partial Economic Area (PEA) market. For this evaluation, we want to see the markets where AT&T’s low band spectrum ownership is less than 45MHz. This would be a PEA market where AT&T would not expect restrictions in the Broadband Incentive Auction (600MHz).

For the Top 50 markets we have the same markets that Joan Marsh indicated in her blog. Also included in the screenshot is amount of low band spectrum that AT&T controls as well as its competitor’s spectrum holdings in the same markets. It is interesting to note that Verizon would be restricted in each of these 6 markets, and T-Mobile only has low band spectrum in 1 of these markets. In addition, we detail how the low band spectrum is divided between cellular spectrum and 700 MHz spectrum.

As we have demonstrated, our data provides similar results to AT&T’s analysis, but it also allows the other national wireless carriers (and over 600 smaller carriers) to be evaluated in the same manner.

Allnet Insights’ Spectrum Ownership Analysis Tool provides county-level spectrum depth and LTE channel configurations, as well as Partial Economic Area (PEA), Economic Area (EA), and Cellular Market Area (CMA) market level spectrum depth evaluations.