Free Shipping On world wide

- HOME

- PRODUCTS

- IN THE NEWS

- SPECTRUM BLOG

- WEB SPECTRUM VIEWER

-

English

-

USD

Free Shipping On world wide

T-Mobile was quite active during the last quarter of 2015 closing deals to acquire low band (700 MHz A and B Block) spectrum. Green areas in the map above reflect areas where T-Mobile controls 12 MHz of spectrum providing for a 5x5 LTE channel. The Blue areas in North Dakota reflect T-Mobile ownership of both the A and B block, enabling the deployment of a 10x10 LTE channel. Below are the transactions that were announced during this time period:

It should be noted that during this same time period, T-Mobile assigned their 700 MHz A-Block spectrum in Alaska to Alaska Wireless Networks. T-Mobile had acquired this spectrum from Triad 700 in late 2014.

Using the 2010 Census Population for each of the US Counties, it can be seen that T-Mobile has over 200 million licensed pops (Population) where they have enough spectrum for a 5x5 low band channel, and 10 thousand pops where they have enough spectrum for a 10x10 low band channel. The 2010 Census set the total US population (states, districts, and territories) at 312 million.

This map and these transactions reflect the Future data set from Allnet Insight's Spectrum Ownership Analysis Tool (January 2016 Version).

How much backhaul capacity do you provide to each cell site for each 10MHz of LTE spectrum?

225 Mbps should be provided for each 10MHz of spectrum (75Mbps per sector)to prevent backhaul from creating a bottleneck.

What percentage of your sites utilize Verizon facilities for backhaul versus alternative backhaul providers?

Verizon has a significant cost advantage in the markets where they provide local telephone service by using internal resources for cell site backhaul.

What is your average monthly backhaul cost per cell site ($/Mbps) for the site using an alternative backhaul provider?

Locations where Verizon utilizes an alternative backhaul provider, the site expense for backhaul will begin to dominate the network cost of service. With the move to data, the site lease (average $1500/mo) is dominated by the backhaul lease ($8000/mo). This becomes more painful as you consider the need for doubling data capacity which could then double your site backhaul expense.

How do you account for the backhaul assets that are provided from your wireline subsidiaries to your wireless business? Are there any charge backs or internal bills based upon usage or capacity?

Now that Verizon has purchased Vodofone’s interest, this is less of an issue. However, concerns still arise that wireline assets are not properly valued for the benefit they provide the wireless business.

Are you deploying RRH (Remote Radio Head) technology? To what percentage of your sites?

Verizon has been the quietest of the national carriers on their plans to deploy RRH technology. It would make sense for Verizon to deploy RRH technology for their AWS and PCS LTE sectors so those sectors can have more similar coverage to their low band (700 MHz) sectors. In markets where Verizon is building an extensive small cell network uses their AWS and PCS frequencies, they will likely not use the RRH technology within the small cell network area.

What percentage of your sites are you converting to RRH (remote radio head) technology?

RRH technology takes radios that typically have been at ground level and places them on the towers behind the antennas. The RRH technology is useful in providing better coverage for the higher frequency spectrum. For AT&T, RRH technology would help mitigate the coverage differential between 700MHz and PCS, 700MHz and AWS, and 700MHz and WCS. If low band coverage (700MHz) were represented by a quarter, and mid band coverage (PCS) by a dime; moving the PCS channel to RRH technology would make the PCS coverage grow to the size of a nickel. This would allow AT&T to have similar capacity across a larger amount of their coverage.

Are you using RRH technology only for your high band spectrum or all spectrum except low band?

Applying RRH technology to low band spectrum in rural areas would fill in coverage holes but increasing coverage in urban areas with RRH technology would increase interference.

What percentage of your customers have a device that will operate on 700 MHz (band 17), AWS (band 4), and WCS (band 30)?

The iPhone 6s has an available version that supports the WCS band, but since not all of AT&T’s customers have a phone that supports their entire LTE spectrum, network coverage and capacity enhancements will not be experienced by the entire user base.

How much back haul capacity do you provide to each cell site for each 10 MHz of LTE spectrum?

To prevent back haul from being a bottleneck, 225 Mbps should be provided for each 10 MHz of spectrum (75Mbps per sector).

What is your average monthly back haul cost per cell site ($/Mbps)?

Site back haul costs would surprise many in the analyst community. When sites only supported voice calls, site leases (land and tower) dominated the operations expense. With the move to data, the site lease (average $1500/mo) is dominated by the back haul lease ($8000/mo). This becomes more painful as you consider the need for doubling data capacity which could then double your site back haul expense.

We are excited to work again with Fierce Wireless to provide their readers with insights into each of the National Carriers deployable spectrum for LTE. As Fierce Wireless indicated in their article, the today's version of the Download Spectrum Maps indicate each carrier's LTE spectrum that would be usable by the latest iPhone 6s. We provided Fierce Wireless with maps indicating downlink spectrum totals for each carrier.

We have created additional maps for each carrier which detail their spectrum LTE channel capabilities for each of their deployable spectrum blocks. You can receive a copy of the 13 map set by emailing info@allnetinsights.com or by signing up for our monthly newsletter at the bottom of our home page (www.allnetinsights.com).

Verizon's LTE spectrum holdings are detailed below:

We also took into account that Verizon is beginning to deploy some of their PCS spectrum for LTE. If Verizon had 20 MHz of PCS spectrum we assumed they would deploy 10 MHz for LTE and if they had 15 MHz of PCS spectrum we assumed they would deploy 5 MHz for LTE. The remainder of the PCS spectrum will continue to be used for voice capacity. If Verizon controlled both blocks of the cellular spectrum, all of their PCS spectrum was available for LTE deployment and if Verizon did not own either block of cellular spectrum, none of their PCS spectrum was available for LTE.

We are proud to announce the release of our September 2015 Spectrum Ownership Analysis Tool. In this release we have updated our data set to include the following August spectrum transactions among others:

Additionally with the September 2015 Spectrum Ownership Analysis Tool, we have added the Channel Block analysis module. This module will detail spectrum holdings for an individual carrier by individual channels. Previously, we have provided analysis modules which detail spectrum holdings by frequency band (700MHz, SMR/Cellular, PCS, AWS, WCS, and BRS/EBS), by band class (Low Band, Mid Band, and High Band), and by LTE band (Band 12, Band 17, Band 5) The new Channel Block analysis module provides the reader with a clear understand of what spectrum is held in a county. This is organized by specific colored channel block.

These graphs detail the peak capacity for downlink files and streaming video for the four major national wireless carriers plus Dish and USCellular. They illustrate the peak capacity on a market-by-market basis. In creating the graphs, I anticipate the usage of each wireless carrier’s total spectrum available, not just the spectrum they have dedicated to LTE at this time. These graphs allow you to see the significant capacity advantage that Sprint will have once they deploy their 2.5GHz spectrum. They also provide a market-by-market comparison of AT&T and Verizon capacity. You can see that AT&T has a capacity advantage versus Verizon in all Top 20 markets except Minneapolis-St. Paul. In addition, you can see the relatively low capacity that T-Mobile is able to offer and the capacity that Dish could provide after they launch a network.

I was able to construct these graphs by using Allnet Insights and Analytics Spectrum Ownership Analysis Tool determine the number of LTE channels that each carrier’s spectrum can support.

Assuming that each LTE channel had the follow achievable LTE Peak Data Rates:

These rates were applied to each of the carriers LTE channels to create a total peak downlink throughput. For all EBS/BRS spectrum (Sprint’s 2.5GHz spectrum), I assumed TDD (Time Division Duplex) LTE operation and each channel’s throughput was reduced to 75% to reflect the 75:25 downlink to uplink ratio for TDD operation. TDD LTE utilizes a single radio channel to both transmit to the mobile device (downlink) and transmit from the mobile device (uplink). In TDD LTE timeslots, similar to the wedges on the Wheel of Fortune, carry either downlink traffic or uplink traffic during that time interval. Since internet traffic is typically 75% downlink and 25% uplink, US operators dedicate 75% of the wedges to downlink and 25% to uplink. Most US spectrum bands are configured for FDD (Frequency Division Duplex) LTE, which utilizes two radio channels, one to transmit to the mobile device (downlink), and one to transmit from the mobile device (uplink).

For this issue of “How does our data compare?” we will look at the following statement from Andy Levin’s blog. Andy is T-Moble’s Senior Vice President of Government Affairs.

"AT&T’s practice of making promises it cannot keep is matched only by its ability to make claims that cannot withstand scrutiny. In the run-up to the 600 MHz auction, for instance, AT&T has derided the spectrum reserve as a “set aside” that “picks winners and losers.”

The claim is laughable: if the reserve is a set-aside, it is a set-aside that AT&T or Verizon can claim in nearly three-quarters of the country. The map below shows the markets where AT&T or Verizon can purchase all the spectrum blocks available in the upcoming 600 MHz auction."

AT&T Plays a Broken Record of Broken Promises – Andy Levin, T-Mobile, Sr VP, Government Affairs

Using Allnet Insights’ Spectrum Ownership Analysis Tool we are able to evaluate AT&T and Verizon’s low band spectrum ownership for all US Partial Economic Area (PEA) markets. We then created a geographic map. This map graphed 4 categories:

The purple areas from Allnet Insights’ map match the white areas from T-Mobile’s map with the exception of a rural PEA in northern Montana. These areas represent the PEA markets that both AT&T and Verizon will be limited in the ability to acquire addition low band spectrum. Clearly from Allnet Insights’ map you can see that there are many additional markets where either AT&T or Verizon is limited, but not both.

The AT&T LTE Channel Band 12 Map is part of a series of 23 maps, which geographically describe the data speed capabilities of the national wireless carriers, including DISH. LTE stands for Long Term Evolution. LTE is a standard for wireless communication of high-speed data for mobile phones and data terminals. The LTE standard covers a range of many different bands, each of which is designated by both a frequency and a band number.

You can think of each of these bands as a highway number that a wireless carrier first needs to build into their network, and needs to enable in each of their smartphones. For example, AT&T would add radios to their cell sites for their 700MHz spectrum1, enabling Band 12, and they would provide an iPhone 6, also supporting Band 12, to their customers. 2

Every telecommunication company has their own information about their service areas and how why they are better than the competition. But how can you determine each carrier’s maximum LTE capability? This is a multi-million dollar question and the answer lies with independent and accurate analysis of each individual national carrier’s LTE coverage. In the featured AT&T LTE Channel Band 12 Map, the channel sizes are delineated between 0, 5, 10, 15, and 20 MHz. The larger channel sizes correspond to faster data speeds. Also included with the channel maps are licensed population breakdowns indicating the licensed population in a specific channel size for the entire US and for the Top 100 CMA Markets.

Allnet Insights & Analytics offer similar maps for each of the wireless carriers, giving you the critical information you require to manage your wireless business with confidence.

1A wireless operators’ most valuable resource is Spectrum. Spectrum is divided into non-overlapping spectrum bands, which are assigned to different cells. Knowing the ownership of the current spectrum for all the mobile carriers and satellite frequency bands would obviously be a high priority. Whereas this information is available, it can be difficult to interpret.

That’s why we developed the Spectrum Ownership Analysis Tool . This powerful, Excel based tool allows users to visualize and analyze the current spectrum ownership for all of the mobile carriers and satellite frequency bands down to a county level.

2AT&T would actually deploy Band 17 which is a subset of Band 12. We used Band 12 for all of the maps to allow easier comparison between wireless carriers using the same spectrum bands. If you were to look at the iPhone specification you would see the corresponding support of Band 17.

For this issue of “How does our data compare?” we will look at the following statement from Joan Marsh’s blog. Joan is AT&T's Vice President of Federal Regulatory.

"For AT&T, the restrictions will predominantly impact our ability to compete for spectrum in urban areas. Indeed, our preliminary analysis suggests that we will be restricted in all Top 50 markets except six (Cleveland, Phoenix, Virginia Beach, Charlotte, Raleigh and Greenville to be exact). The restrictions will therefore directly impact our ability to serve customers in the most data hungry markets like NY, Los Angeles, Chicago, San Francisco, Baltimore-DC, Philadelphia, Boston and Dallas."

T-Mobile’s Magenta Herring – Posted by Joan Marsh (AT&T)

Using Allnet Insights’ Spectrum Ownership Analysis Tool we are able to evaluate AT&T’s low band spectrum ownership for all US Partial Economic Area (PEA) market. For this evaluation, we want to see the markets where AT&T’s low band spectrum ownership is less than 45MHz. This would be a PEA market where AT&T would not expect restrictions in the Broadband Incentive Auction (600MHz).

For the Top 50 markets we have the same markets that Joan Marsh indicated in her blog. Also included in the screenshot is amount of low band spectrum that AT&T controls as well as its competitor’s spectrum holdings in the same markets. It is interesting to note that Verizon would be restricted in each of these 6 markets, and T-Mobile only has low band spectrum in 1 of these markets. In addition, we detail how the low band spectrum is divided between cellular spectrum and 700 MHz spectrum.

As we have demonstrated, our data provides similar results to AT&T’s analysis, but it also allows the other national wireless carriers (and over 600 smaller carriers) to be evaluated in the same manner.

Allnet Insights’ Spectrum Ownership Analysis Tool provides county-level spectrum depth and LTE channel configurations, as well as Partial Economic Area (PEA), Economic Area (EA), and Cellular Market Area (CMA) market level spectrum depth evaluations.

Many have grown accustomed to using the FCC Spectrum Dashboard for quick and relatively simple access to spectrum ownership data. This was never a complete solution for spectrum ownership analysis because many frequency blocks (AWS-H, AWS-3, and AWS-4) were never available for query. There have been several blocks of data that have entirely disappeared (700MHz – D block) or been so reduced in quantity that what is left is highly questionable.

Recently, I went to the FCC Spectrum Dashboard to download a large block of spectrum data for analysis. To receive a large data file, the FCC has historically sent a link to a user input email address where the data can be downloaded. After 3 unsuccessful attempts, to receive the email links, I called the FCC support line and was informed that feature was indeed broken and would not be fixed. The customer support representative also indicated that the data available on the site had not been updated since 7/7/2014, over a year ago.

I think we can declare the FCC Spectrum Dashboard dead as a spectrum ownership tool. Since Allnet Insights tracks all spectrum transactions related to the mobile carrier frequencies, we know that since July 9, 2014 over 350 applications have been submitted changing the ownership or leasing on nearly 700 call signs. These numbers don’t include any of new AWS-3 call signs which include an additional 1,614 call signs. In all, the FCC Spectrum Dashboard has incorrect data for nearly 2000 call signs.

Fortunately, AllNet Insights’ Spectrum Owners Analysis Tool and its National Carrier reports continue to provide the industry leading information on spectrum ownership through our carefully managed spectrum ownership database This database maintains the current licensee, lease, and future licensee for every block of US wireless carrier spectrum.

| Final Daily Digest

| Initial Daily Digest

| Market

| Call Sign

| Current Channel

| Proposed Channel

|

| Oklahoma City, OK

| KSBI(TV)

| 51

| 23

| ||

| Rome, GA

| WPXA(TV)

| 51

| 31

| ||

| Kansas City, MO

| KPXE-TV

| 51

| 30

| ||

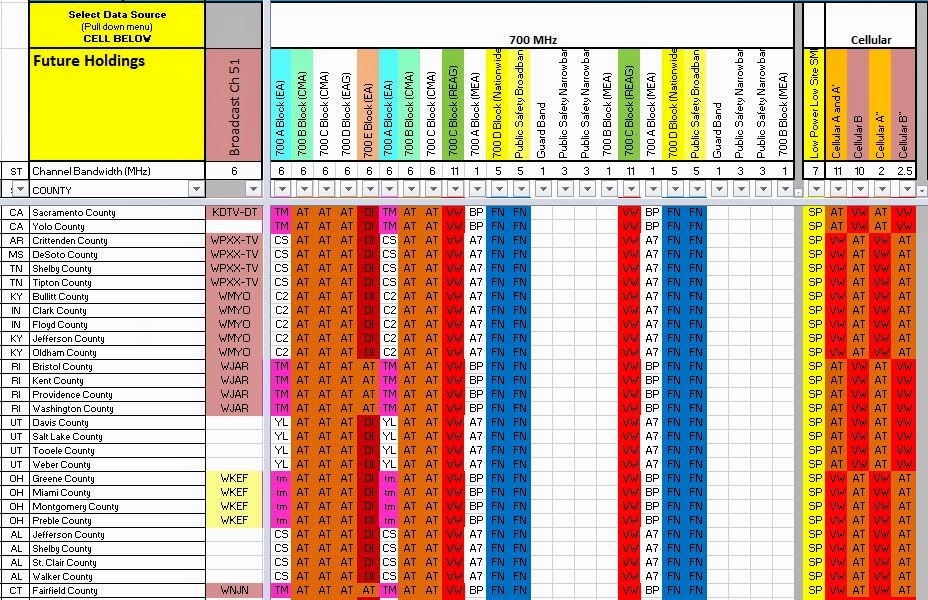

| Dayton, OH

| WKEF(TV)

| 51

| 18

| ||

| Denver, CO

| KCEC(TV)

| 51

| 26

| ||

| Longview, TX

| KCEB

| 51

| 26

| ||

| Lansing, MI

| WLAJ-TV

| 51

| 25

| ||

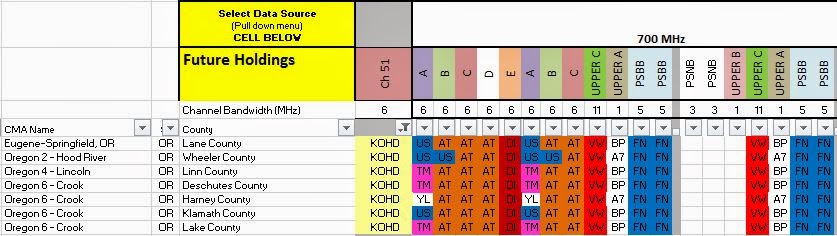

| Bend, OR

| KOHD

| 51

| 18

| ||

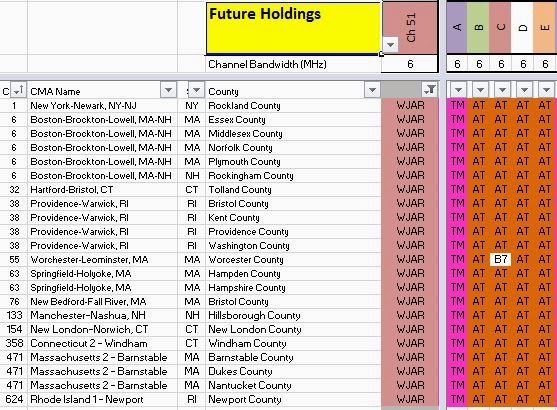

| Providence, RI

| WJAR(TV)

| 51

| 50

|

| Final Daily Digest | Initial Daily Digest | Market | Call Sign | Current Channel | Proposed Channel |

| Oklahoma City, OK | KSBI(TV) | 51 | 23 | ||

| Rome, GA | WPXA(TV) | 51 | 31 | ||

| Kansas City, MO | KPXE-TV | 51 | 30 | ||

| Dayton, OH | WKEF(TV) | 51 | 18 | ||

| Denver, CO | KCEC(TV) | 51 | 26 | ||

| Longview, TX | KCEB | 51 | 26 | ||

| Lansing, MI | WLAJ-TV | 51 | 25 | ||

|

| Bend, OR | KOHD | 51 | 18 | |

| Providence, RI | WJAR(TV) | 51 | 50 |

| Final Daily Digest | Initial Daily Digest | Market | Call Sign |

Current Channel |

Proposed Channel |

| 12/13/2013 | Oklahoma City, OK | KSBI(TV) | 51 | 23 | |

| 9/4/2014 | Rome, GA | WPXA(TV) | 51 | 31 | |

| 9/4/2014 | Kansas City, MO | KPXE-TV | 51 | 30 | |

| 12/23/2014 | 9/18/2014 | Dayton, OH | WKEF(TV) | 51 | 18 |

| 12/16/2014 | 10/17/2014 | Denver, CO | KCEC(TV) | 51 | 26 |

| 12/8/2014 | Longview, TX | KCEB | 51 | 26 |

| Final Daily Digest | Initial Daily Digest | Market | Call Sign |

Current Channel |

Proposed Channel |

| 12/13/2013 | Oklahoma City, OK | KSBI(TV) | 51 | 23 | |

| 9/4/2014 | Rome, GA | WPXA(TV) | 51 | 31 | |

| 9/4/2014 | Kansas City, MO | KPXE-TV | 51 | 30 | |

| 12/23/2014 | 9/18/2014 | Dayton, OH | WKEF(TV) | 51 | 18 |

| 12/16/2014 | 10/17/2014 | Denver, CO | KCEC(TV) | 51 | 26 |

| 12/8/2014 | Longview, TX | KCEB | 51 | 26 |